Activix

Activix  AutoTrader

AutoTrader  Black Book

Black Book  CarGurus

CarGurus  Equifax

Equifax

.png)

You already know negative equity is killing deals. The trade is upside down, the lender's LTV cap leaves no room for rollover, and your team burns 45 minutes penciling a unit the customer was never going to get approved on anyway. Then the appointment no-shows, and the whole cycle starts again.

The problem isn't that negative equity is unavoidable—it is manageable. The problem is that most desks are trying to solve a financing math problem with a sales process that was built before financing math mattered at the lead level.

In our experience working with dealerships across Canada, there are 4 factors that sales

managers, desk managers, and F&I managers need to get right to consistently close negative equity deals without sacrificing gross:

1. Start with a credit-qualified lead, not a raw form fill

Knowing the equity gap before the first call changes everything about how you structure the conversation, the unit, and the deal.

2. Quantify the negative equity gap against real approval constraints

LTV, PTI, and lender booking limits are the actual boundaries of the deal. You need those numbers before you pull a unit off the lot.

3. Use approval constraints to define a "buyable" inventory set—automatically

Manually cross-referencing lender terms against 200+ units is where time dies and deals fall apart. A good system does this in seconds.

4. Desk a structure that protects gross while fitting lender rules

Solving negative equity isn't the same as discounting. Frontend, reserve, and backend all need to be optimized together—not traded off against each other.

After years of watching dealerships lose deals they should have closed—and building AVA™ from the ground up with dealer input—we designed AVA™ MatchBook to address all four of these factors end-to-end.

Here's how each one works in practice.

1. Start With a Credit-Qualified Lead (Not a Raw Form Fill)

Credit-Qualified Leads: Know the Equity Gap Before Your BDC Makes the First Call

The single biggest reason negative-equity deals stall isn't the deal structure—it's that the desk doesn't see the full picture until they're already 30 minutes into a pencil. By then, the customer has an expectation, the salesperson has made promises, and the desk is trying to work backwards from a number that was never realistic.

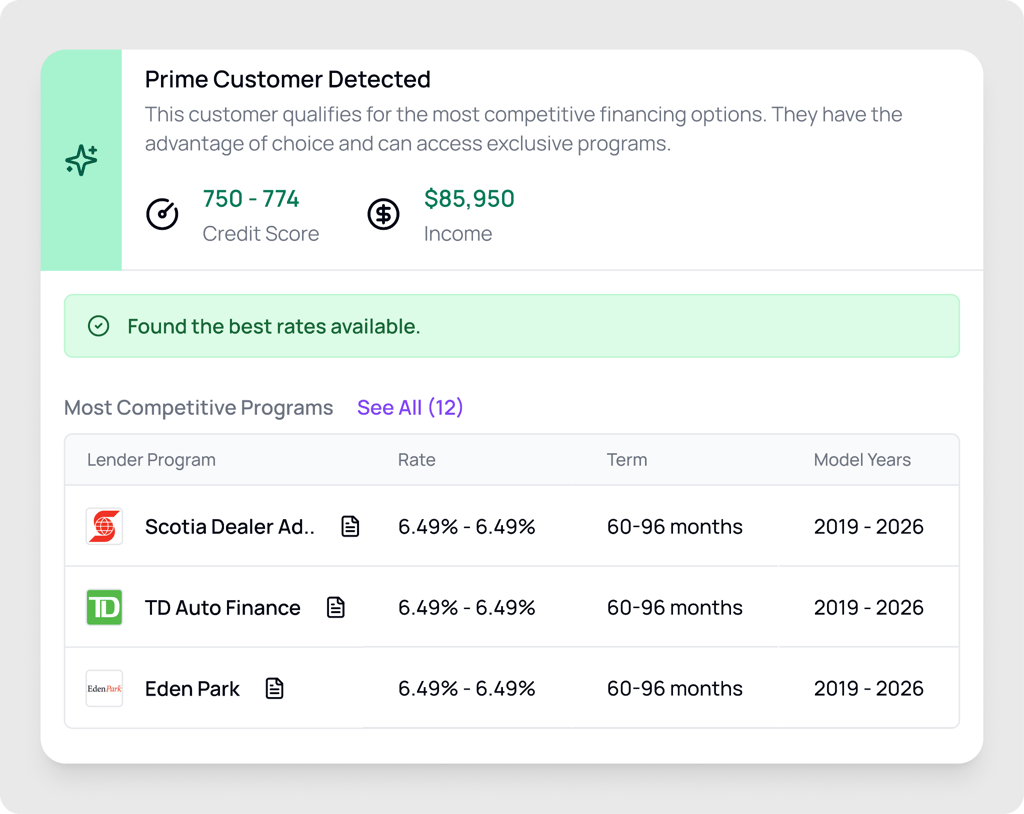

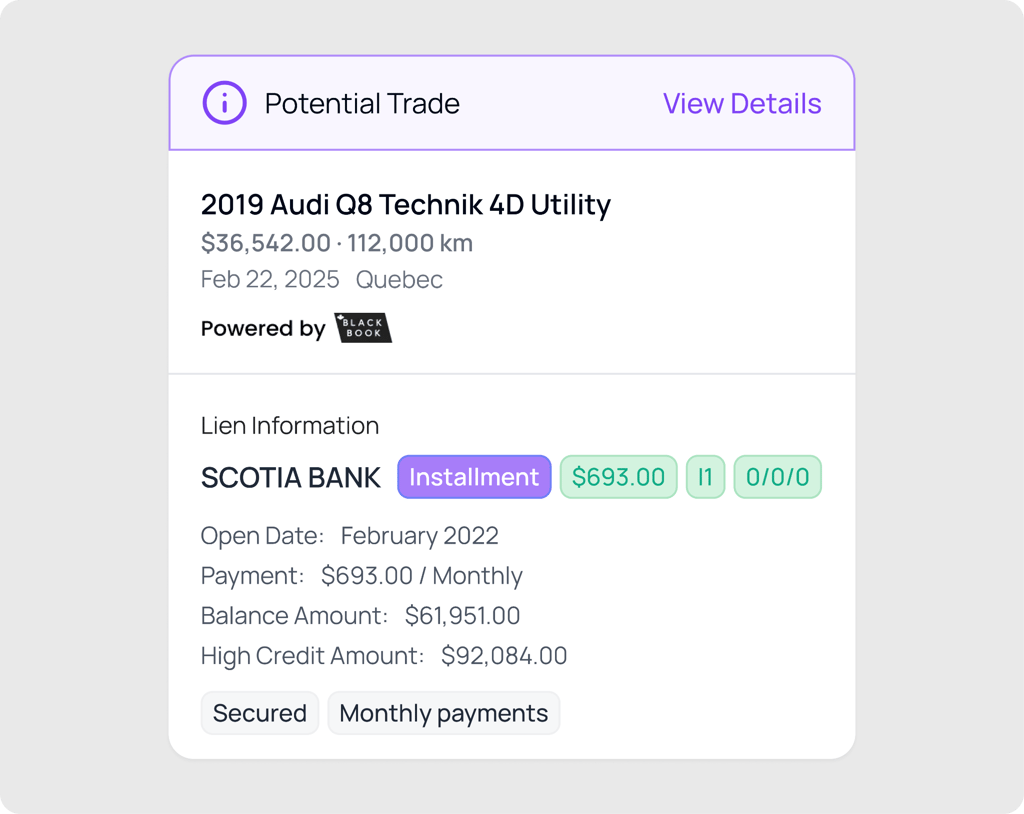

AVA™ Credit changes where that information enters the process. When a customer submits a credit application through your website or via a BDC-sent link, AVA runs a soft-pull Equifax check in real time—no impact to the customer's score—and builds what we call a Credit- Qualified Lead (CQL). If the customer also indicates their trade-in vehicle during the credit application, the CQL is enriched with trade data automatically. By the time that lead hits your portal, your team already sees:

- Credit score and tier (e.g., Subprime 580)

- Current vehicle, remaining balance, and current payment

- Trade-in value (powered by Canadian Black Book)

- Negative equity flag and dollar amount (e.g., -$6,000)

For example, say a lead comes in on a Saturday morning. Your BDC rep opens the AVA portal and sees the lead tagged SUBPRIME | NEGATIVE EQUITY -$6,000. Instead of setting a vague appointment and hoping the desk can figure it out, the rep knows immediately: this customer owes $28,000 on a vehicle worth $22,000. That's the gap the deal has to absorb.

That one data point—visible before the first call—changes the entire conversation. The BDC can set a realistic expectation. The desk can pre-select units. The appointment has a purpose.

For many dealerships, if a BDC rep saw a lead with a trade, they'd set the appointment, note "has a trade," and leave the desk to discover the equity problem live on the floor. That costs everyone time and kills show rates when customers feel blindsided by numbers that don't work.

In AVA, the equity position is visible the moment the lead is created—so the right person acts on the right information before a single call is made.

2. Quantify the Negative Equity Gap Against Real Approval Constraints (Saving You Hours of Dead-End Pencils)

Knowing there's a $6,000 negative equity gap is step one. Knowing what that gap means for lender approval is where most desks still struggle.

From our experience building this platform alongside F&I managers, the majority of desk managers don't want another spreadsheet or another login. They want to answer three questions at a glance:

1. What is this customer's actual buying power? — Not what they want to spend, but what a lender will approve given their credit tier, LTV cap, and PTI threshold.

2. How much of the negative equity can be rolled into the deal? — And which lenders will allow it, at what terms?

3. What price band does that leave for the vehicle? — So the desk knows which units are even worth pulling before they waste floor time.

AVA™ Credit Insights surfaces exactly this. When you open a CQL in the portal, the credit data isn't just a score—it's a deal coach. You can see the credit tier, the approval range it typically supports, and the trade equity position all in one view.

For example, say your desk manager opens the lead for a customer with a 580 Subprime score, a $28,000 payoff, and a trade worth $22,000. That's -$6,000 in the hole. Most lenders at that tier will cap LTV at 120–125% of book. That means the vehicle the customer buys needs to have enough book value to absorb both the purchase price and the rolled-in negative equity without blowing the LTV ceiling.

Without this math done upfront, your desk is guessing. They pull a $35,000 SUV, pencil it, send it to the lender, and get a conditional approval that doesn't work because the book value doesn't support the total advance. That's 45 minutes gone and a customer who's now frustrated.

With the equity gap and credit tier visible from the lead, the desk can skip straight to step three: finding units that actually fit.

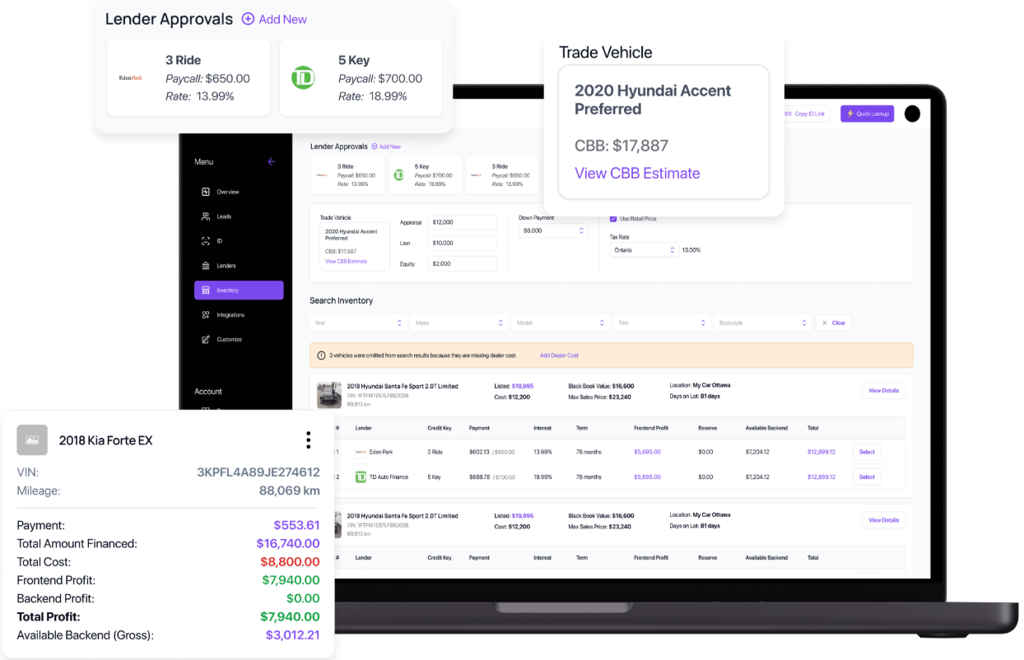

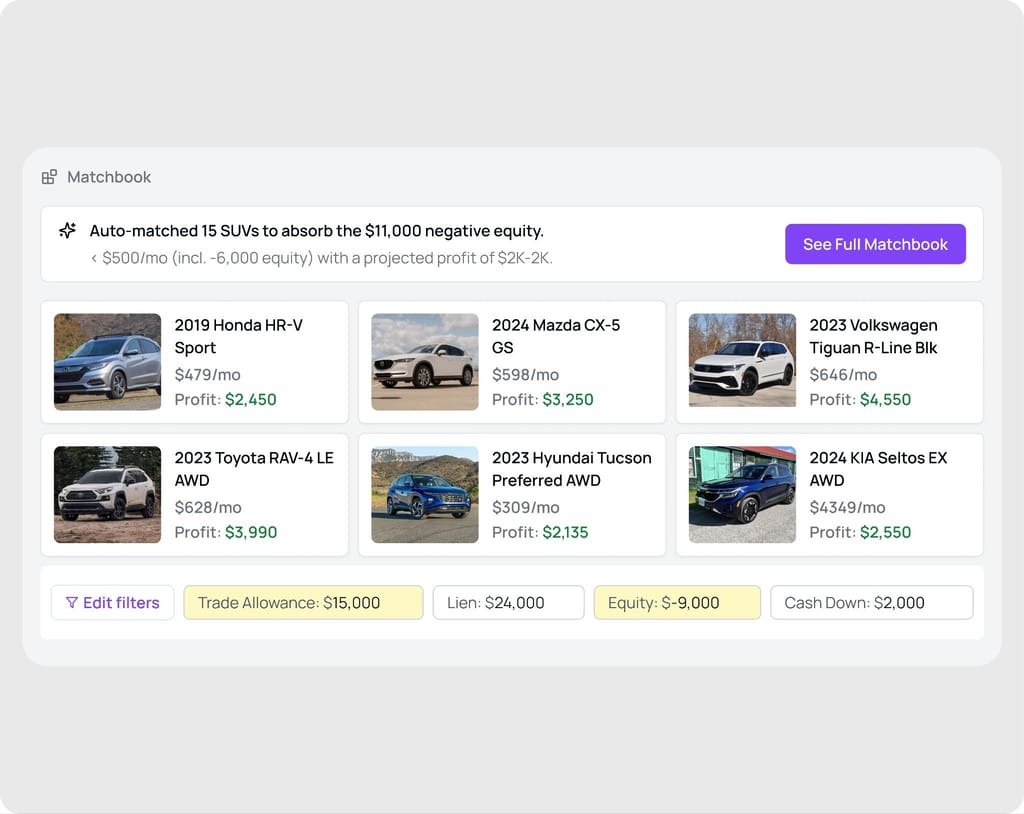

3. Match Approval Constraints to In-Stock Inventory Automatically (Without Manual Cross-Referencing)

This is where most dealerships are still doing things the hard way.

Even when a desk manager knows the credit tier and the equity gap, matching those constraints to specific in-stock units is a manual process. They're pulling up inventory on one screen, checking book values on another, running payment estimates in their head or on a calculator, and trying to remember which lenders will and won't touch certain mileage or vehicle age thresholds. It takes 20–40 minutes per deal. And it's wrong often enough to cost real money.

AVA™ MatchBook was built specifically to eliminate that manual step.

Here's how it works: enter the trade-in details and the lender approval parameters, and MatchBook instantly scans your DMS-synced inventory and surfaces only the units that fit within the lender's approval terms. Every vehicle in the results list has already passed the LTV check, the mileage filter, the vehicle age threshold, and the booking limit—all using Canadian Black Book data, the same data Canada's major banks use to set their own parameters.

AVA® pulls soft-inquiry credit and full bureaus before F&I, so deals get structured to fund. Take the tour.

For example, say your desk is working a deal for a customer with a Subprime 580 score, -$6,000 negative equity, and a lender approval that caps total advance at $30,000 with a 120% LTV limit. That means you need to find a unit where:

- Vehicle price → fits within the approval advance after rolling in the $6,000 gap

- CBB book value → supports the total advance at 120% LTV

- Mileage → within the lender's acceptable range (e.g., under 120,000 km)

- Vehicle age → within the lender's model year window

- Payment → fits the customer's PTI at the approved rate and term

MatchBook filters your entire inventory against all five criteria simultaneously and returns a ranked list of eligible units in seconds. The desk doesn't have to touch a spreadsheet or crossreference a lender guide.

"The craziest thing that I just realized and the point of this whole thing is the car that it showed me that we would make the most money on was a 130k older vehicle. And I would have never in a million years picked that car, period."

— Shawn Cyr, MyCar

That quote captures exactly what happens when you let the data lead. The unit that works for the lender, absorbs the negative equity, and maximizes profit is often not the unit a desk manager would have pulled intuitively. MatchBook finds it in under 60 seconds.

For many F&I managers, if a desk asked them to identify the best unit for a subprime buyer with negative equity, they'd say "give me a few minutes" and spend the next half hour manually checking inventory, running book values, and calling the lender rep. That's if they don't just give up and show the customer something that won't get approved.

In AVA™ MatchBook, that same task takes under a minute—and the result is a ranked list of units the lender will actually approve.

4. Desk a Structure That Protects Gross (Without Sacrificing Frontend to Make the Deal Work)

Yes, this article is about fixing negative equity. But a good inventory matching system should also protect your gross—not just find a unit that technically fits the lender's parameters.

Why? Because the instinct when a deal is hard is to discount. Drop the price, cut the frontend, do whatever it takes to make the payment work. That's how negative-equity deals become negative gross deals. And that's a pattern that compounds fast across a month.

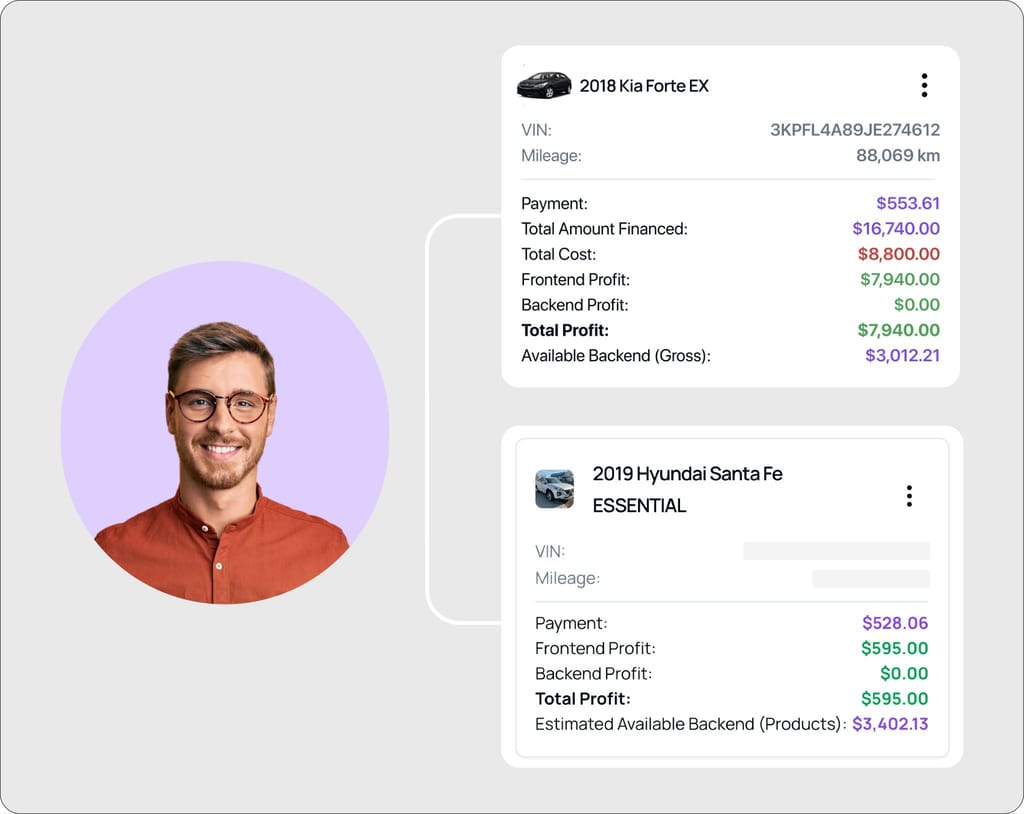

AVA™ MatchBook's Profit Optimization Engine changes that calculus. For every unit in the matched results, MatchBook calculates:

- Frontend profit — based on your asking price vs. cost

- Reserve — estimated backend reserve based on rate and term

- Backend profit potential — F&I product opportunity based on deal structure

So the desk isn't just seeing "this unit fits the lender." They're seeing "this unit fits the lender and generates $2,400 in frontend plus an estimated $800 in reserve." That's the difference between closing a deal and closing a profitable deal.

Now, you might wonder: can't we just figure this out in our desking tool? Yes—but only after you’ve already identified the unit, which is the step that currently takes 30-40 minutes of manual work. MatchBook does the unit identification and the profit calculation together, so the desk is never choosing between speed and margin.

It also removes the data discrepancy problem. When book values, lender caps, and profit estimates all come from the same integrated source—Canadian Black Book data powering both the matching logic and the profit calculations—you're not reconciling numbers from three different tools that were pulled at different times.

For example, in a typical MatchBook results view, a desk manager can see a ranked list of instock units sorted by backend profit potential, with each unit showing the total advance, the CBB book value, the estimated payment at the approved rate, and the frontend gross—all color-coded by approval confidence. The highest-profit unit that fits the lender's terms rises to the top automatically.

In short, the desk can walk into a conversation with a specific unit, a specific payment, and a specific profit structure—without having spent 40 minutes getting there.

See It Working: A Full Negative-Equity Deal in Under 60 Seconds

Here's what the complete workflow looks like when all four factors are in place:

Step 1 — CQL arrives with equity flag visible

A lead comes in through your website. AVA Credit runs a soft-pull Equifax check. The portal shows: Subprime 580 | Trade: 2019 Acura TLX | Payoff: $28,000 | Trade Value: $22,000 | Negative Equity: -$6,000.

Step 2 — BDC sets a structured appointment

Instead of a vague "come in and we'll see what we can do," the BDC rep uses the credit tier and equity data to set a realistic expectation: "We've already looked at your credit and your trade situation. We have a few units in stock that work within your budget—let's get you in to look at them."

Step 3 — Desk runs MatchBook before the customer arrives

The desk manager enters the trade details and lender approval parameters into MatchBook. In under 60 seconds, they have a ranked list of 4–6 in-stock units that fit the LTV cap, the mileage threshold, and the payment constraint—with profit estimates for each.

Step 4 — Customer arrives to a pre-structured deal

Instead of a 90-minute back-and-forth while the desk figures out what unit to show, the customer is walked directly to units that work. The conversation starts with the vehicle, not the math.

Step 5 — F&I closes on a profitable structure

The F&I manager works from a deal that was already optimized for reserve and backend opportunity. No frontend was sacrificed to make the payment work. The lender approves on the first submission.

This is what a repeatable system looks like—not a one-off save, but a consistent process that works the same way every time a negative-equity lead comes through the door.

Ready to Stop Losing Negative-Equity Deals You Should Be Closing?

For more information on how AVA™ MatchBook works—and how dealerships are using it to close subprime and negative-equity deals faster and more profitably—request a MatchBook demo or explore the full AVA™ platform.

The math on manual matching is straightforward: at 40 deals per month requiring matching, the average dealership loses $18,600/month in labor costs and missed opportunities. That's $223,200 annually—before counting the deals that simply never closed because the right unit was never found in time.

MatchBook pays for itself the first week you use it.