Activix

Activix  AutoTrader

AutoTrader  Black Book

Black Book  CarGurus

CarGurus  Equifax

Equifax

It's Saturday afternoon. A walk-in just test-drove a RAM 1500 he's serious about, but you have no idea what he can actually afford, which lender will approve him, or whether the deal you're about to structure will fund. The old options are: ask him to fill out an online credit app while he waits (he won't), or burn a hard inquiry on his bureau and hope the first submission lands (it probably won't).

There's a third option now. In under 30 seconds, from your desk, you can pull the customer's full credit bureau as a soft inquiry no impact to his score, no online form, same depth of data your lender will use to adjudicate the deal. That's a dealer-initiated soft pull, and until recently it didn't exist for Canadian dealers.

Most dealerships today are only running the older type: the consumer-initiated soft pull, where the customer fills out a form on the dealership website and a credit score range lands in the CRM. That tool still has its place but if it's the only soft-pull tool you're running, you're leaving the higher-value job (structuring deals at the desk) on the table.

This guide is for Sales Managers and Operations Managers trying to figure out:

- How to actually run a dealer-initiated soft pull at your store (step-by-step)

- How to run a consumer-initiated soft pull off your website (step-by-step)

- The real differences between the two and when to reach for which

- The compliance and consent rules in Canada specifics, not hand-waving

- What it costs and what it saves

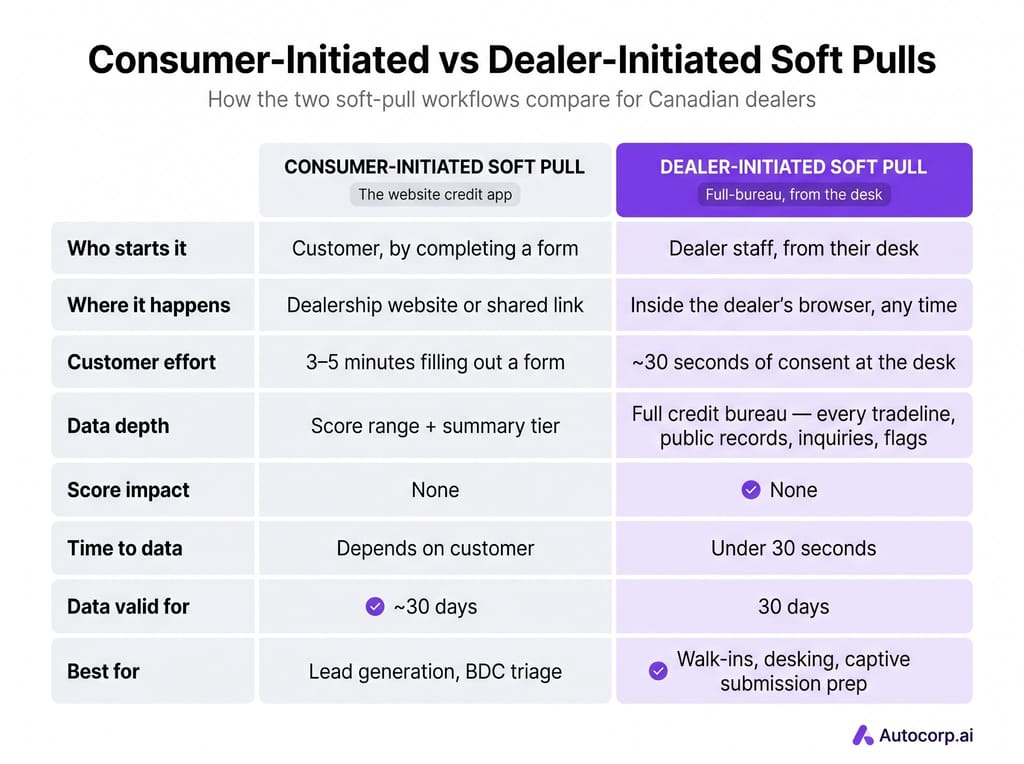

The two types of soft pulls, side by side

When dealers say "soft pull" they usually mean the website credit app. The customer enters their info, the system runs a soft inquiry against the bureau, and the dealer gets a credit score range back. Useful tool, but it's not the only one available, and most dealerships don't realize there's a second option.

Here's how the two compare on the things that actually matter to a sales floor:

Both are soft pulls. Both are PIPEDA-compliant when done correctly. Both leave the customer's score untouched. But the job each one does in your store is completely different.

Why the consumer-initiated pull, by itself, isn't enough

The consumer-initiated soft pull is excellent at one thing: turning anonymous website traffic into named, credit-qualified leads. Your BDC gets a prioritized call list. Marketing knows which campaigns drive prime vs. subprime traffic. You stop wasting hours on phantom leads who were never going to buy.

But it has three structural limits any sales manager will recognize:

- It requires the customer to take action. No form completion, no pull. Walk-ins who haven't been on your site? You get nothing. Customers who started the form and bailed at the income question? Nothing.

- It returns a score range, not a file. A range like "675–699" tells your BDC who to call first. It doesn't tell your desk whether to send the deal to TD or RBC, what term to run, or whether the customer is carrying two open auto loans that will trigger a debt-to-income decline.

- The data is bureau-specific. If your website form runs against Equifax and the customer's captive lender pulls TransUnion, you're flying blind on the file your deal will actually be adjudicated against.

The dealer-initiated soft pull closes all three gaps. No form to complete. Full bureau file. The bureau your lender actually uses.

Start here: how to run a dealer-initiated soft pull (the full-bureau workflow)

This is the workflow that lets your team pull a complete credit file on a customer in front of them in under 30 seconds, without a hard inquiry, so the deal gets structured correctly the first time.

What needs to be in place before the first pull

Three things have to be set up before your team can run one:

- A dealer compliance approval with the bureau. TransUnion (and Equifax for that matter) requires every dealer running their own pulls to complete a standard dealer compliance review. This verifies your dealer license, your corporate registration, your PIPEDA consent workflow, and provisions your subscriber code. Plan on 3–5 business days. If you're going through Autocorp, the paperwork is handled end-to-end as part of Co-Driver onboarding, your team doesn't fill out bureau forms directly.

- A consent capture workflow. PIPEDA requires informed, documented consent before any credit inquiry soft or hard. For dealer-initiated pulls, that consent happens at the desk. It can be verbal-and-logged or signed on a tablet, but it has to be timestamped and stored. The most common compliance failure is staff running the pull first and capturing consent later. Don't.

- A tool that's authorized to run the pull. You need software that's an approved bureau integrator, with the consent capture, the pull, the audit log, and the data display all in one workflow. AVA™ Co-Driver is the Canadian tool built for this. It lives in a Chrome extension that overlays your DMS, desking, and CRM, so your team doesn't have to leave the screen they're already on.

The walkthrough

1. Install the AVA™ Co-Driver Chrome extension.

Co-Driver is browser-based. It overlays whatever platform your team is already using DMS, DealerTrack, CRM, desking tool, so there's no new system to learn. Once installed, the AVA™ launcher appears across every page. If the extension isn't detected, the portal prompts you to install it:

2. Capture consent at the desk.

Before the pull, get consent. Co-Driver ships with a built-in consent prompt — verbal language a salesperson can read aloud, or a tablet-signable version. Once captured, it's timestamped and stored on the customer's record. If a customer ever disputes the inquiry, the audit trail is there.

3. Open the customer's record or deal jacket in whatever system you're working in. If CoDriver can read the customer's name, DOB, and address from the page, it pre-fills. If not, you punch them in manually, the same three fields you'd enter for a hard pull.

4. Run the TransUnion soft pull.

Click "Run TU Soft Pull" in the Co-Driver panel. The pull goes out, the bureau responds, the file is parsed and surfaced in your AVA™ portal. Total time: under 30 seconds.

5. Read the file.

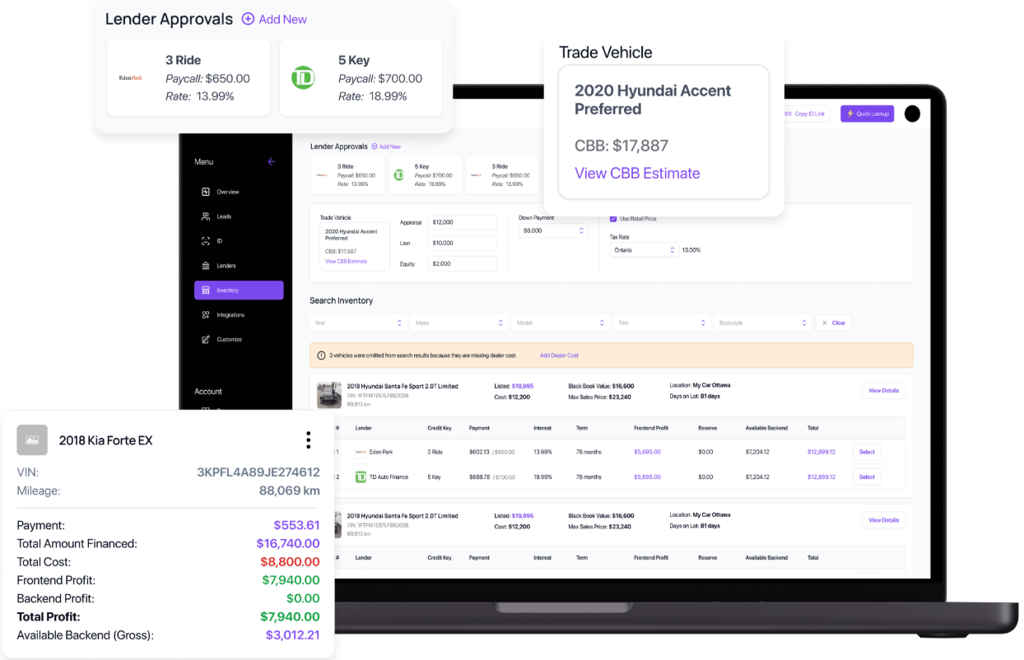

This is the part that separates dealer-initiated pulls from consumer-initiated ones. You're not looking at a score range, you're looking at the full TransUnion bureau:

- CreditVision score — the exact number your captive lender will see

- Every tradeline — balances, credit limits, payment patterns, MOP codes (the bureau's payment-history shorthand), current status

- Public records — bankruptcies, collections, judgments, registered items

- Inquiry history by industry — every recent pull, so you can spot rate-shoppers and shadow apps before submission

- Fraud and file flags — high-risk alerts, ID mismatches, consumer warnings

- Employment and address history — for stip-readiness on subprime deals

6. Structure the deal against the file, not against a guess.

This is the payoff. Instead of submitting to four lenders and hoping one approves, your desk submits to the one or two you know will book the deal. If MatchBook is part of your stack, you can match the customer's actual buying power to specific units on your lot in the same workflow.

7. The pull is valid for 30 days.

If the customer comes back to upgrade, change units, or finalize after thinking it over, you don't need to re-pull until the 30-day window closes.

Back to the Saturday afternoon walk-in

That RAM 1500 customer from the intro? Here's how it plays out with a dealer-initiated pull.

He filled out your website credit app last week. Equifax came back at 612 borderline subprime, and your usual lenders for that tier are TU-primary. You could submit and burn a hard inquiry to find out which one will book him. Or your team can run TransUnion in Co-Driver in 30 seconds before submitting anything.

You run the pull. CreditVision comes back at 648 same customer, different bureau, different story. Three open tradelines, all current, low utilization. One paid collection from 2021, now closed. No recent auto inquiries (so he's not shadow-shopping). Four years at the same employer.

Now you know two things: which captive will see this deal favourably, and exactly how to structure it. Your team submits to the one lender you're confident about, with a term and down payment built around what the file actually shows. The deal funds the first time. The customer doesn't get a hard inquiry on his file for a deal that wasn't going to land.

This is the kind of deal that, before dealer-initiated pulls existed, you would have either lost or burned a hard inquiry to chase.

How to run a consumer-initiated soft pull (the website credit app workflow)

This is the version most dealers already know, so we'll keep it tight. The primary goal is: capture credit-qualified leads off your website and into your CRM, without ever asking for a hard pull.

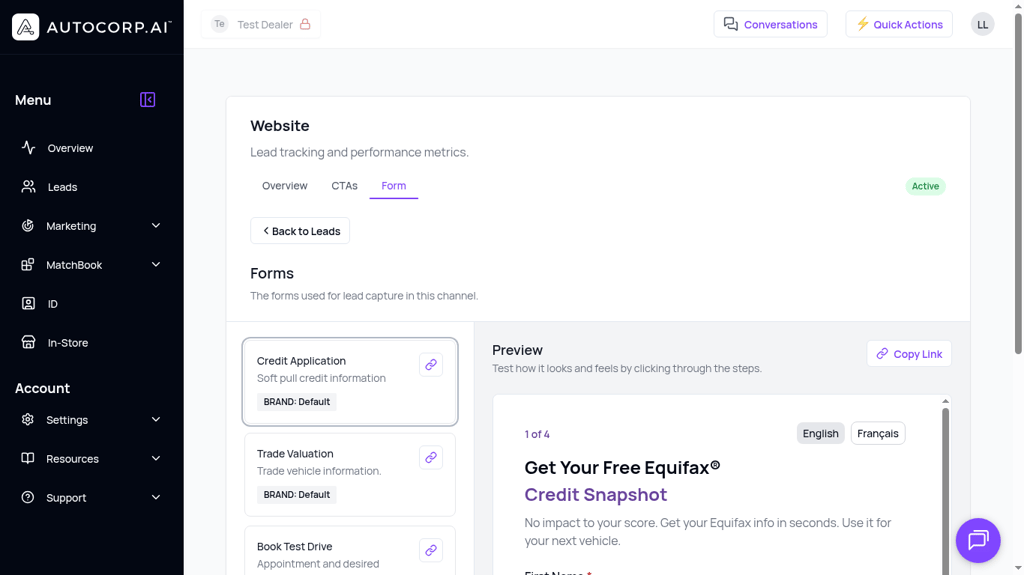

1. Add a soft-pull credit application to your website.

You need a form that lives on your VDPs, SRPs, and a dedicated landing page. It should be bilingual (English/French) if you're in Canada, mobile-first, and short enough that the average shopper will actually finish it. Three to four steps is the sweet spot any longer and you'll see drop-off spike at the income question.

AVA® tire le crédit par consultation douce et les bureaux complets avant le F&I, pour structurer des transactions qui se financent. Faites la visite.

The customer needs to provide enough information for the bureau to match their file: full name, date of birth, current address, and consent language that explicitly authorizes the soft inquiry.

In the AVA™ portal, this is the Credit Application form that ships pre-built with every plan — you copy the link, drop it on your site, and start capturing leads:

2. Route every completion to your CRM with the credit data attached.

A soft pull that sits in a separate tool is a soft pull your BDC will ignore. The lead needs to land in the system your team already lives in CRM, DMS, ADF feed with the score, the tier, and any trade or vehicle interest information attached.

This is where the workflow usually breaks for dealers building their own setup. The bureau API speaks one language, your CRM speaks another, and stitching them together typically takes a developer. Off-the-shelf tools like AVA™ handle this with ADF / DMS / PBS integrations out of the box.

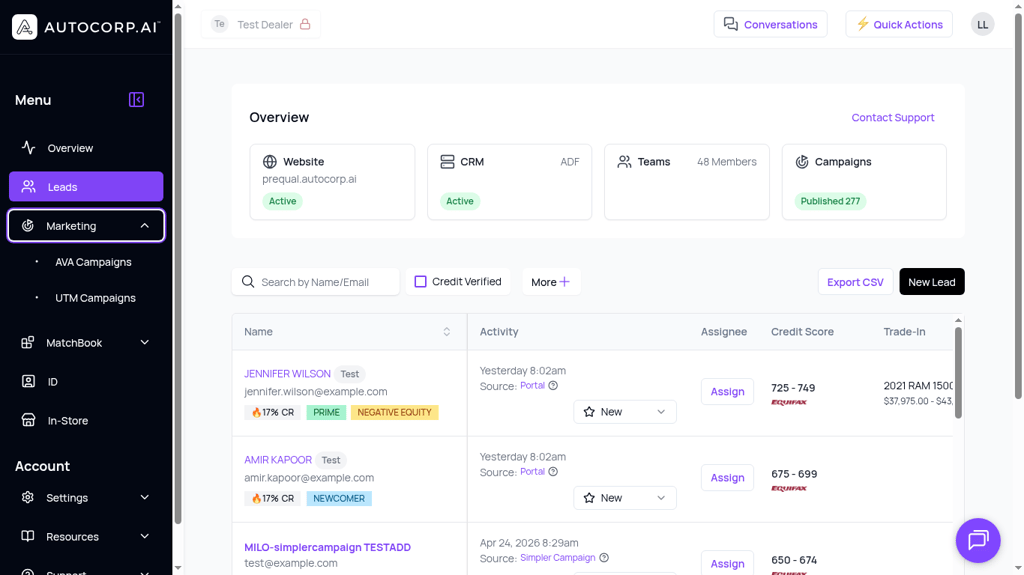

3. Prioritize the BDC call list by credit tier.

Once leads are flowing, the workflow is: every morning (or in real time, if your team is fast), the BDC pulls up the lead list, filters by Credit Verified, and works highest-tier leads first. Prime customers get called within minutes. Near-prime gets routed to your subprime specialist. Thin file / newcomer gets a different script.

Here's what that prioritized list looks like with credit tiers, score ranges, and trade equity flags all visible at a glance:

4. Use the data, don't just collect it.

This is the part most dealerships skip. A credit-qualified lead in your CRM is worthless if your sales team doesn't change their approach based on it. Build a simple playbook: which tier gets which call script, which tier gets routed to which salesperson, which tier triggers a same-day appointment offer vs. a nurture sequence.

That's the consumer-initiated workflow. It runs in the background, generates a steady stream of credit-qualified internet leads, and answers the question "who do I call first?"

What it doesn't answer is "this customer is in front of me right now how do I structure this deal?" That's the dealer-initiated workflow above.

Compliance and consent in Canada what's actually required

Most articles about dealer soft pulls hand-wave on compliance. Here's the specific answer.

Both types of soft pulls require informed consent. That's PIPEDA, and it applies regardless of who initiates the pull. The difference is where the consent is captured.

- Consumer-initiated pulls capture consent inside the form. The customer reads the disclosure, checks the box, signs the consent language. The form completion is the consent record.

- Dealer-initiated pulls capture consent at the desk, verbally (logged) or signed on a tablet. The tool you use should timestamp and store the consent record automatically. If you're using a tool that doesn't, you have a compliance hole.

Both types require a bureau-approved compliance setup. Equifax and TransUnion both require dealers (or their software vendors) to be approved subscribers. If you're working with a Canadian-focused tool like AVA™, this is handled by the vendor — you're operating under their compliance umbrella, with your dealership-specific subscriber code provisioned during onboarding. If you're building your own integration, you'll be filing the paperwork directly with the bureau, which is a longer road.

The "can I just pull anyone's credit?" question is the one every dealer asks first. The answer is no, and you wouldn't want to even if you could — the audit trail on bureau inquiries is exact, and unauthorized pulls are how dealers lose their bureau access. The correct goal isn't "skip consent." It's "make the legitimate consent flow as fast and frictionless as possible so it never slows down a deal." Thirty seconds at the desk, signed on a tablet, done.

When to reach for which type

If you have both running, here's how the workflow shakes out in the field:

Consumer-initiated pulls run in the background. Website traffic flows through your credit app form 24/7. Marketing campaigns route to the same form. Leads land in your CRM with credit tiers attached, your BDC works them by priority, and you get a steady stream of credit-qualified appointments coming through the door.

Dealer-initiated pulls run at the moments that matter most to closing deals:

- A walk-in who hasn't completed your online credit app. Run Co-Driver before the test drive. Now you can match them to inventory they can actually afford.

- Desking a deal. Pull the full TU file before you build the deal structure. Saves a round trip when the first submission comes back declined.

- Equifax data is borderline. Cross-bureau check on TransUnion to see if a TU-primary lender will tell a different story.

- Captive submission prep. Your captive (Honda Financial, Toyota Credit, GM Financial) decisions on TransUnion data. See what they'll see before you submit.

- Subprime structuring. Full tradeline visibility, public records, and inquiry history are what separate deals that fund from deals that come back declined or with bigger down payment requirements than the customer can swing.

- BDC follow-up on incomplete website credit apps. Customer started the form, bailed at the income question pull at the desk so the BDC has something to work with on the call.

Most stores end up using both. The consumer-initiated tool fills the funnel. The dealer-initiated tool closes the deals.

What it costs (and what it costs you not to do this)

For context against the alternatives Canadian dealers are running today:

- A hard pull through DealerTrack: roughly $4–$8 per inquiry depending on your bureau contract plus the cost to the customer relationship if they find out you pulled them before they were ready to commit, and the cost of the wasted submission if it comes back declined.

- An Equifax consumer-initiated soft pull through AVA™ Credit: $7.95/pull on any AVA™ plan.

- A TransUnion dealer-initiated full bureau through AVA™ Co-Driver (Early Bird): $4.99–$6.99 per pull, platform fee waived during the Early Bird window.

The math gets interesting fast. If your store burns three hard inquiries a month on deals that don't fund — a conservative estimate at most stores — one $4.99 Co-Driver pull that keeps even one of those from happening pays for itself the same morning. And the time saved (no callbacks, no resubmissions, no chasing a deal that was never going to land) compounds across every walk-in your team sees.

Frequently asked questions

Does a soft pull affect the customer's credit score?

No. Equifax Canada confirms that soft inquiries don't impact credit scores Soft inquiries don't appear on the version of the credit report lenders see, and they don't move the FICO or CreditVision score.

How long is soft pull data valid for in Canada?

TransUnion dealer-initiated soft pulls through Co-Driver are valid for 30 days. Equifax consumer-initiated soft pulls have a similar window. Hard pulls are valid for 15 days.

Do I need a separate TransUnion account to run dealer-initiated pulls?

No, if you're using a Canadian-approved tool like AVA™ Co-Driver. The vendor handles the TransUnion subscriber setup and dealer compliance approval as part of onboarding (typically 3–5 business days). If you're building direct, you'll work with the bureau directly.

Can my team run a dealer-initiated soft pull on a customer who hasn't given consent?

No, and a properly-built tool won't let them. Consent capture is required before every pull, with a timestamped audit trail.

What's the difference between Equifax and TransUnion in Canada?

Different lenders decision on different bureaus. Some Canadian captives are TU-primary, some are Equifax-primary. When you can see both files, you stop submitting deals to the lender whose bureau makes the file look weaker than it actually is.

Is dealer-initiated soft pull available outside Canada?

AVA™ Co-Driver’s TransUnion integration is currently a Canadian product.

The bottom line for your sales floor

There are two soft-pull workflows available to Canadian dealers right now, and they do different jobs. The consumer-initiated website credit app fills your funnel with credit-qualified leads and gives your BDC a prioritized call list. The dealer-initiated full-bureau pull, run from your desk in under 30 seconds, gives your finance team the same data the lender uses to adjudicate, before you submit a single hard inquiry. One feeds the pipeline. The other closes deals.

If you're a Sales Manager or Operations Manager doing the math on this, the case for dealer-initiated is straightforward:

- Closes the walk-in gap. Customers who never filled out your online form (most of them) finally get qualified before the test drive instead of after the deal falls apart.

- Cuts the rework. Submitting deals against a guess generates declines, callbacks, and resubmissions. Submitting against the actual bureau file the lender sees doesn't. That's hours back to your team every week.

- Reduces fraud exposure. Fraud and file flags surface on the bureau before the deal goes to F&I — you catch synthetic identities and stolen IDs before they cost you a chargeback.

- Protects the customer relationship. No more "I just need to run your credit" conversations on deals that aren't going to fund anyway. The hard inquiry only happens when you know the deal will land.

The objection most dealers raise is reasonable: another new system, another training rollout, another vendor relationship. It's worth being direct about that. AVA™ Co-Driver lives in a Chrome extension that overlays the tools your team already uses, DealerTrack, your DMS, your CRM, so there's nothing new to log into and almost nothing to learn beyond "click the button when the customer is at your desk." The bureau compliance paperwork is handled for you. Your CSM gets you live in 3–5 business days.

If you want to see what the full TransUnion file looks like in the portal before you commit, book a 20-minute walkthrough of AVA™ Co-Driver. We'll pull a sample file together so you can see exactly what your finance team will be working with.

The dealers running both workflows aren't doing anything mysterious they've just stopped accepting "fly blind or burn a hard pull" as the only two options on their sales floor.