Activix

Activix  AutoTrader

AutoTrader  Black Book

Black Book  CarGurus

CarGurus  Equifax

Equifax

Sales efficiency has become one of the most important performance drivers in automotive retail. With tighter margins, rising acquisition costs, and more digitally savvy buyers, dealerships can no longer afford to treat every lead the same. Time spent chasing low quality or unready shoppers directly impacts closing rates and team productivity.

This is where credit qualified leads make a meaningful difference. By identifying buyers who are both interested and financially positioned earlier in the journey, dealerships can focus effort where it matters most and improve outcomes across the sales funnel.

Key Takeaways

- Credit qualified leads are car shoppers who show buying intent and complete a preliminary credit check (usually a soft pull).

- Soft pull credit checks typically do not impact a shopper’s credit score, so dealers can gather early financing insight with less friction.

- Credit qualified leads help dealerships prioritize outreach, reduce time spent on unresponsive or unfinanceable leads, and improve sales team productivity.

- Early credit insight helps improve closing rates and deal speed by catching financing issues earlier in the process.

- Sharing credit readiness data earlier helps sales and finance align on realistic options, which can reduce last minute surprises for the buyer.

What are credit qualified leads

Credit qualified leads are shoppers who have demonstrated buying intent and have completed a preliminary credit evaluation, typically through a soft pull credit check. Unlike traditional internet leads, these buyers are not just browsing inventory or requesting general information. They have taken a step that indicates readiness to explore financing and move forward realistically.

Because soft pull credit checks do not impact a customer’s credit score, they allow dealerships to gather valuable financial insight without creating friction or hesitation. This data helps separate casual interest from serious opportunity.

Why traditional lead volume hurts efficiency

Many dealerships still measure success by lead volume. While high lead counts can look positive on reports, they often hide inefficiencies within the sales process.

Sales teams spend hours calling, emailing, and texting leads that are unresponsive, unqualified, or unable to secure financing. This leads to frustration, slower response times for serious buyers, and burnout among sales staff.

Credit qualified leads shift the focus from volume to value. When sales teams know which shoppers are financially viable, they can prioritize outreach more effectively and reduce wasted effort.

Faster prioritization and smarter follow ups

One of the most immediate benefits of credit qualified leads is improved prioritization. When a lead includes credit readiness data, sales teams gain clarity on who should be contacted first and how quickly.

Buyers who have completed a soft pull credit check and engaged with financing options often respond faster and are closer to a purchase decision. Sales managers can assign these leads strategically, ensuring experienced staff handle high intent opportunities.

Follow ups also become more relevant. Instead of generic check ins, conversations can focus on realistic payment ranges, vehicle options that fit the buyer’s profile, and next steps toward approval.

Improved closing rates and deal velocity

Efficiency is not just about saving time. It is about closing more deals with the same or fewer resources.

Credit qualified leads typically convert at higher rates because financial barriers are identified early. Sales teams are less likely to invest time in deals that collapse late due to credit issues. This reduces rework, renegotiation, and deal fatigue.

By addressing financing readiness upfront, dealerships shorten the path from first contact to delivery. Faster deal velocity improves inventory turn and overall sales performance.

Better alignment between sales and finance teams

Credit qualified leads also improve collaboration between sales and finance departments. When credit data is available earlier, finance managers can prepare more accurate options and avoid last minute surprises.

Sales teams enter discussions with clearer expectations, while finance teams receive customers who are already educated and realistic about their situation. This alignment reduces friction, speeds up approvals, and creates a smoother experience for the buyer.

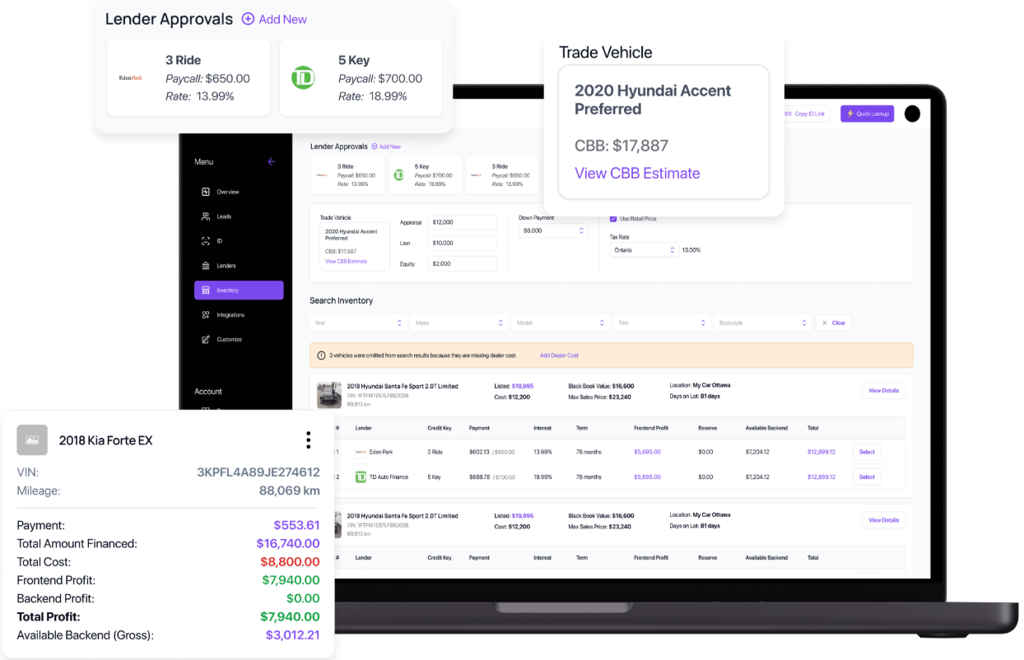

Solutions like AVA Credit are designed to generate credit qualified leads by integrating soft pull credit data directly into the sales workflow. This allows both sales and finance teams to work from the same information and focus on deals that are most likely to fund.

More transparent and trusted customer experiences

Trust plays a critical role in modern car buying. Buyers want transparency, especially around financing. When credit conversations are delayed until late in the process, customers often feel surprised or misled.

Credit qualified leads help dealerships introduce financing discussions earlier and more openly. Buyers understand their position, explore options confidently, and feel more in control of the process.

This transparency builds credibility and reduces objections. Customers are more receptive to recommendations when they feel the dealership is guiding them honestly rather than pushing them through a rigid process.

Reduced stress on sales teams

See how 650+ dealerships use AVA® to surface credit-qualified buyers before they sit down at the desk.

Sales efficiency is also about sustainability. Teams that constantly chase unqualified leads experience higher stress and lower morale.

Working credit qualified leads gives salespeople confidence that their effort has a higher chance of success. Conversations become more productive, wins feel more consistent, and performance becomes more predictable.

This improves job satisfaction and helps retain top talent, which is an often overlooked benefit of improving lead quality.

Using data to continuously improve performance

Credit qualified leads generate valuable insights beyond individual deals. Over time, dealerships can analyze patterns related to lead sources, engagement behaviour, and closing outcomes.

For example, dealers may find that buyers who complete a soft pull credit check within the first 24 hours convert at significantly higher rates. These insights can inform marketing strategies, follow up timing, and staffing decisions.

Data driven refinement helps dealerships continuously improve efficiency rather than relying on static processes.

Integrating credit qualified leads into existing workflows

Adopting credit qualified leads does not require reinventing the sales process. The most successful dealerships integrate credit data into their existing CRM, BDC, and sales workflows.

The key is consistency. Teams must understand how to interpret credit signals, prioritize leads accordingly, and communicate clearly with customers. Training and alignment ensure the data is used effectively rather than ignored.

Platforms like AVA™ Credit support this integration by surfacing credit readiness without adding complexity or disrupting the customer experience.

Why credit qualified leads matter more than ever

As competition intensifies and buyer expectations continue to rise, dealerships must operate smarter, not harder. Credit qualified leads provide a practical way to improve efficiency without increasing workload.

By focusing on buyers who are ready and able to purchase, dealerships reduce wasted effort, close deals faster, and create better experiences for both customers and staff.

Sales efficiency is no longer about doing more. It is about doing what matters most. Credit qualified leads make that possible.

Frequently Asked Questions About Credit Qualified Leads

What is a credit qualified lead in auto sales?

A credit qualified lead is a shopper who has shown buying intent and completed an initial credit evaluation, often through a soft pull credit check. This separates serious buyers from casual shoppers and helps dealers focus on leads that are more likely to close.

Does a soft pull credit check affect a customer’s credit score?

The article states that soft pull credit checks do not impact a customer’s credit score. That makes it easier to introduce early financing conversations without adding as much hesitation.

Why do credit qualified leads improve sales efficiency at dealerships?

They reduce wasted time on low quality leads and help teams focus follow ups on buyers who are financially viable. With credit readiness data, sales teams can prioritize outreach, make conversations more relevant, and avoid deals that fall apart late due to financing issues.

How do credit qualified leads improve closing rates and deal velocity?

They surface financing barriers earlier, so sales teams spend less time on deals that collapse at the end. This reduces rework and renegotiation, shortens the time from first contact to delivery, and can improve inventory turn.

How do credit qualified leads help sales and finance work better together?

When credit information is available earlier, finance can prepare more accurate options, and sales can set clearer expectations with the buyer. This alignment can speed up approvals and reduce friction during the handoff from sales to finance.