In today’s automotive market, the role of a finance manager has never been more critical, or more complex. Rising fraud, tighter lending conditions, and more informed customers mean that every deal carries more risk than it did just a few years ago.

For dealerships, reducing that risk isn’t just about compliance. It’s about protecting time, improving deal quality, and ensuring more transactions actually get funded.

The good news is that with the right processes and tools in place, finance managers can significantly reduce exposure while improving efficiency across the board.

Automotive retail has evolved quickly. More of the buying journey now happens online, customers are sharing sensitive information digitally, and fraud tactics have become more sophisticated.

At the same time, lenders are becoming stricter. Deals that once would have been approved are now being scrutinized more closely.

This creates a challenging environment where finance managers must:

Without a strong process, it’s easy to waste hours on deals that fall apart late, or worse, expose the dealership to fraud or compliance issues.

One of the biggest mistakes dealerships still make is waiting too long to verify identity.

Many stores rely on outdated methods like photocopying driver’s licenses or visually inspecting IDs. These approaches leave room for:

The earlier identity is verified, the lower the risk.

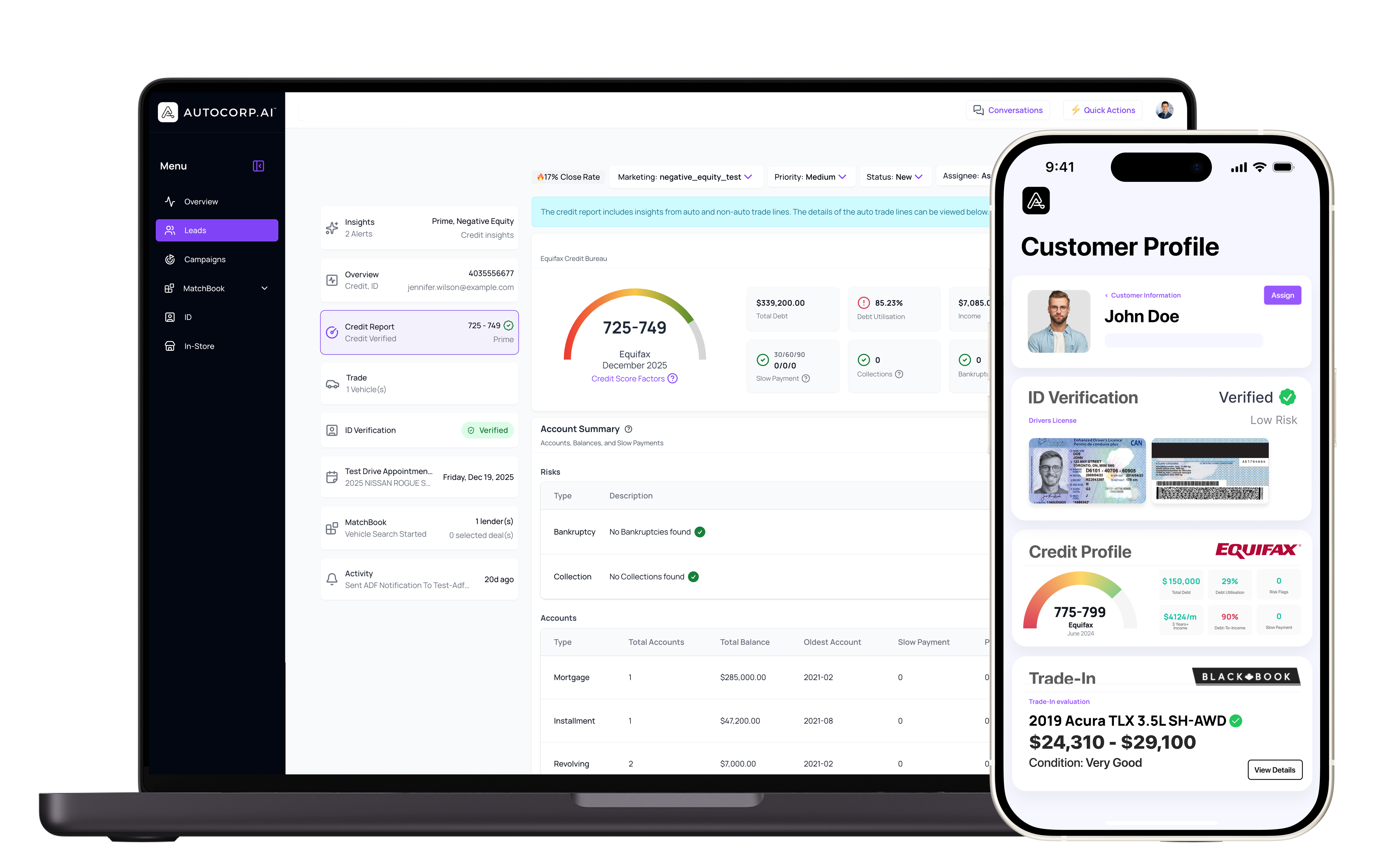

Tools like AVA™ ID allow dealerships to digitally verify a customer’s identity in seconds using secure, real-time validation. Instead of relying on manual checks, finance managers can confidently confirm that the person they’re working with is legitimate before moving forward.

This simple shift can prevent hours of wasted time and significantly reduce fraud exposure.

Another major risk comes from working deals without understanding the customer’s financial position.

Without early credit insight, finance managers and sales teams often:

Soft credit pull technology solves this problem.

With tools like AVA™ Credit & VeriDrive™, dealerships can access key credit insights without impacting the customer’s score. This allows teams to understand buying power early and structure deals accordingly.

When you know a customer’s credit range upfront, you can:

Inconsistent processes create risk.

If every finance manager handles deals differently, it becomes harder to maintain compliance, track performance, and ensure accuracy.

A standardized process should include:

Standardization not only reduces errors but also improves efficiency. Your team spends less time figuring out what to do next and more time moving deals forward.

Paper-based processes are not just inefficient, they’re risky.

Storing physical copies of sensitive customer information increases the chances of:

Digital tools reduce these risks by centralizing and securing information.

By moving away from manual workflows and toward digital verification and data capture, finance managers can create a more secure and streamlined process.

In a high-pressure environment, it’s easy to focus on pushing as many deals as possible. But not all deals are worth pursuing.

Low-quality deals often result in:

By prioritizing qualified buyers early, finance managers can focus on deals that are more likely to close and fund.

This is where tools like VeriDrive™ play a key role. By combining identity verification and credit insights in one process, dealerships can quickly determine whether a deal is viable before investing significant time.

Regulations around automotive financing continue to evolve, and non-compliance can be costly.

Finance managers need to stay informed on:

Using modern tools helps ensure compliance is built into your process rather than treated as an afterthought.

For example, digital identity verification solutions like AVA™ ID provide a more secure and compliant alternative to manual checks.

Risk often increases when there’s a disconnect between the sales floor and the finance office.

If sales teams are bringing forward unqualified or misinformed customers, finance managers are forced to fix problems late in the process.

Better alignment means:

Sharing tools like soft credit insights and verification data across teams helps create a more unified and efficient workflow.

Reducing risk in the finance office isn’t about slowing down the process, it’s about improving it.

When finance managers have better information earlier, they can:

By combining best practices with modern tools like AVA™ ID or VeriDrive™, dealerships can move faster while reducing exposure at every stage of the deal.

In 2026, the most successful finance departments won’t be the ones working the hardest, they’ll be the ones working the smartest, with the right systems in place to support every decision.