Even in a digital first buying world, test drive walk-ins remain one of the strongest buying signals a dealership can get. When a customer walks onto the lot asking for a test drive, intent is already there.

The problem is not traffic. The problem is timing. Too many dealerships wait until late in the process to talk about credit, which often leads to wasted time, stalled deals, and frustrated customers.

By connecting ID verification and credit early, dealerships can turn walk-ins into credit qualified leads without adding pressure or friction.

Key Takeaways

Most test drive processes follow the same pattern. A customer walks in, chooses a vehicle, provides ID, and heads out for a drive. Credit is discussed later, often after pricing and negotiations begin.

When credit comes up late, two things usually happen:

This leads to dropped deals, awkward conversations, and longer sales cycles.

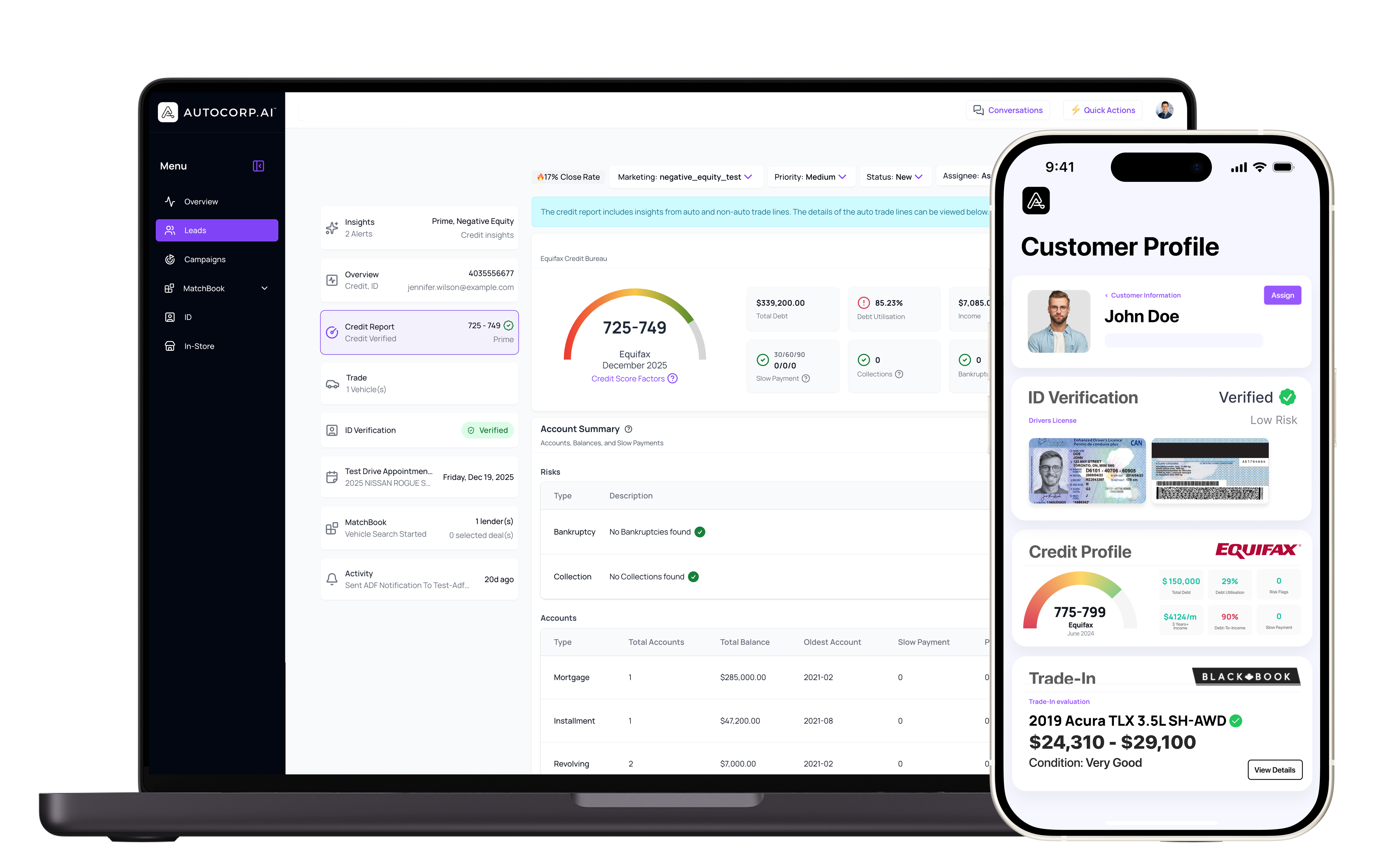

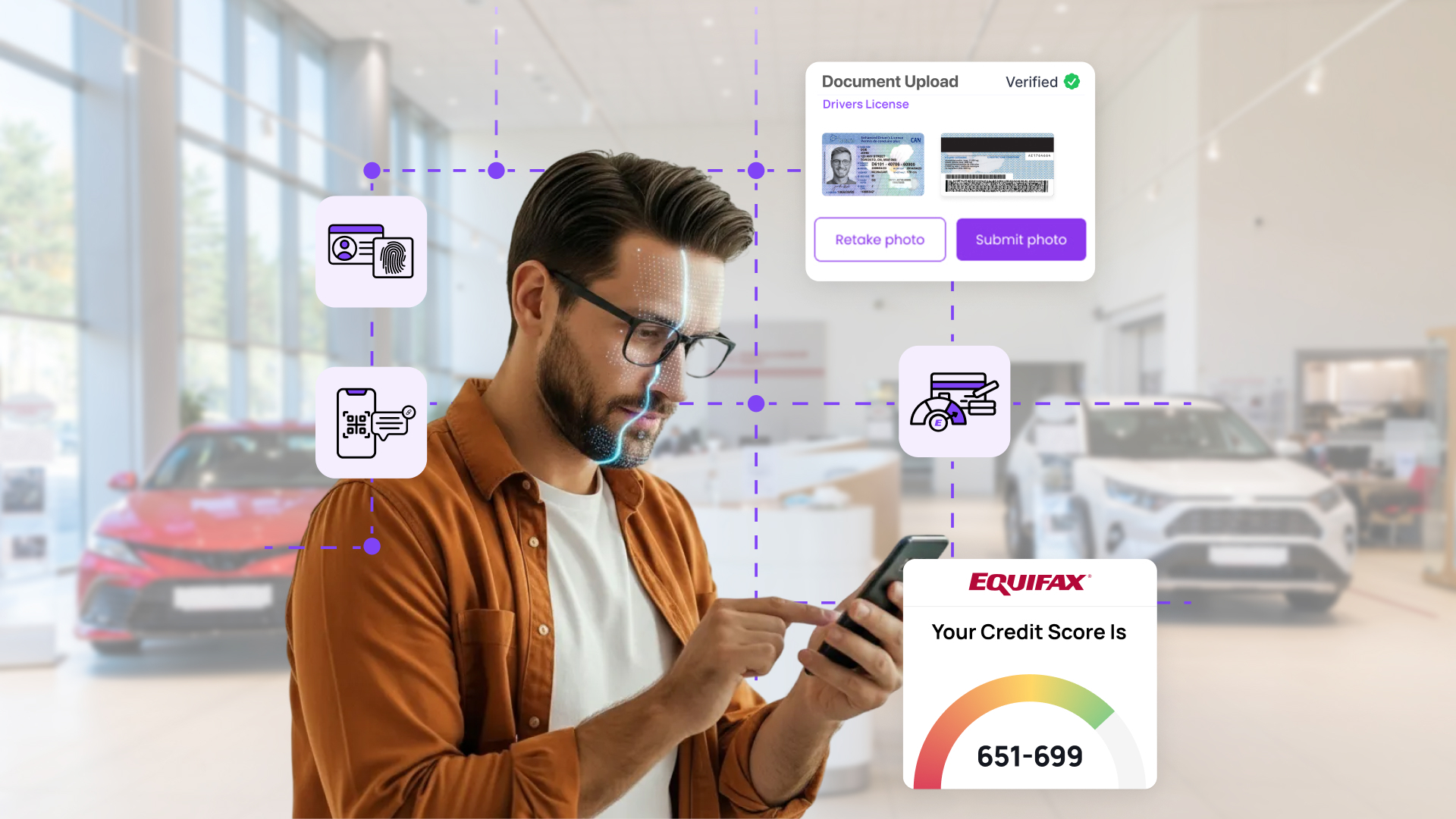

ID verification already happens during test drives for compliance and safety reasons. The opportunity is what happens immediately after.

Modern ID verification tools allow customers to securely verify their identity on their own device in minutes. Once complete, the flow does not need to stop.

At the end of ID verification, customers can be offered the option to view their no impact credit score. Because trust is already established, this step feels logical, not intrusive.

Why Customers Say Yes to Credit at This Stage

Timing matters. During a test drive, interest is high and curiosity is strong. Customers want to know if the vehicle they like actually fits their budget.

When customers understand that checking their credit will not affect their score, hesitation drops. Instead of avoiding the topic, many customers welcome the clarity.

Common motivations include:

This opt-in transforms a walk-in into a credit qualified lead.

Once a customer completes ID verification and views their credit profile, sales teams gain clarity immediately.

Instead of guessing, sales teams can:

Deals move forward faster and with fewer surprises.

The strongest results come when ID and credit are treated as standard, not optional add-ons.

When every test drive includes verified ID and an optional no impact credit check, dealerships naturally build a pipeline of credit qualified leads.

This approach reduces wasted ups, improves close rates, and creates a smoother experience for both customers and staff. If you want to learn more about connecting ID and credit, check out VeriDrive!

How do you bring up credit during a test drive without adding pressure?

Use the ID check as the bridge. After the customer completes ID verification on their device, offer an opt in to view a no impact credit score. The timing feels normal because trust is already established and the customer is already engaged in the process.

What does “no impact credit check” mean for the customer?

It means the customer can view their credit information without affecting their credit score. When shoppers know it will not lower their score, they are more open to seeing where they stand before talking about payments.

Why do late credit conversations cause deals to fall apart?

When credit comes up after pricing and negotiation, sales teams may have already invested time in a deal that is not workable. Customers also feel surprised when financing shows up late, which creates tension, delays, and more walk aways.

What changes for the sales team when credit is handled early?

They can match customers to vehicles that fit their likely payment range, discuss payments with confidence, and reduce back and forth with desk managers. The deal moves faster with fewer surprises.