Activix

Activix  AutoTrader

AutoTrader  Black Book

Black Book  CarGurus

CarGurus  Equifax

Equifax

The Finance and Insurance (F&I) process is one of the most important profit centers in any dealership. It’s where gross margins grow, customers finalize major buying decisions, and trust is either built, or broken. Yet, even experienced F&I managers can fall into patterns that reduce sales, damage customer confidence, and hurt overall satisfaction.

Key Takeaways

- Overloading buyers with every product at once kills decisions, keep it simple and relevant.

- Personalize the F&I pitch with CRM, credit insights, and pre-qualification, not a one-size script.

- Build value before price, tell clear benefit stories and use real examples.

- Meet buyers online, integrate digital F&I tools and virtual options to reduce friction.

- Lead with transparency to build trust, explain costs clearly and follow up after delivery.

Today’s buyers are more informed, more skeptical, and more digitally connected than ever before. They expect transparency, speed, and personalization throughout every step of the car-buying journey. If your F&I presentations don’t meet those expectations, even small missteps can cost you both revenue and repeat business.

Below are five of the most common mistakes dealers make during F&I presentations and how to fix them.

1. Overwhelming Customers With Information

One of the biggest challenges in F&I is balancing compliance with clarity. Too often, managers try to cover every product, policy, and protection plan all at once. The result? Information overload.

When buyers feel overwhelmed, they tune out. Studies show that customers presented with too many choices experience “decision fatigue,” making them more likely to decline every option rather than make a confident purchase.

How to fix it:

- Prioritize relevance. Tailor the presentation to the customer’s actual needs and ownership habits. For example, a high-mileage commuter might find value in a service contract, while a short-term lessee probably won’t.

- Use plain language. Avoid jargon like “GAP” or “etching” without explaining what those terms mean. Keep it conversational and benefit-driven.

- Simplify the menu. Group related products and start with your top two or three recommendations before expanding further.

When F&I managers simplify their approach, customers feel more confident and are more likely to say “yes.”

2. Treating Every Customer the Same

Not every buyer has the same needs, credit profile, or expectations. Yet many F&I presentations still follow a rigid, one-size-fits-all script. This generic approach not only feels impersonal but can also miss opportunities to address unique customer motivations.

How to fix it:

- Leverage data. Use your CRM, digital retailing tools, and credit insights to personalize each presentation. Knowing whether a buyer values convenience, affordability, or protection helps you focus on what matters most.

- Segment by buyer type. A first-time buyer will respond differently than a loyal repeat customer. Adjust tone, pace, and product recommendations accordingly.

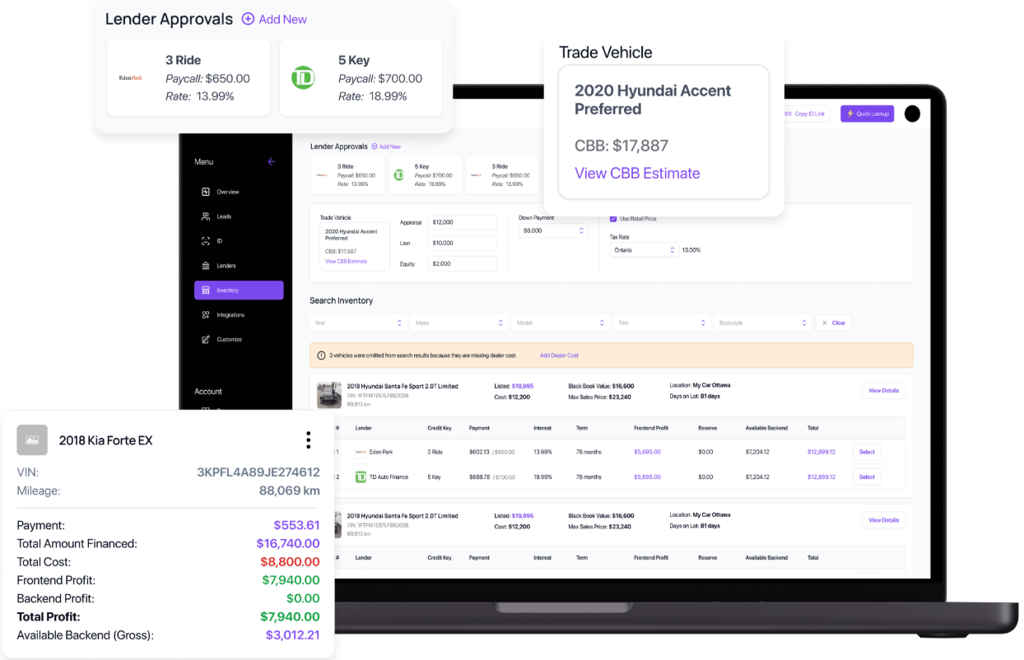

- Use digital pre-qualification tools. Platforms like AVA™ Credit by Autocorp.ai allow dealerships to pre-qualify customers earlier in the process, giving F&I managers a head start on tailoring finance options before the buyer enters the office.

Personalization builds trust, demonstrates attentiveness, and improves both CSI scores and product penetration rates.

3. Failing to Build Value Before Price

Many F&I managers rush to the numbers. They present the cost of a protection plan or warranty before clearly explaining its value. This “price-first” strategy often triggers resistance, especially from cost-sensitive buyers who haven’t yet seen the benefit.

How to fix it:

- Lead with value stories. Instead of saying, “This warranty costs $1,800,” start with, “This coverage saves our average customers $2,000–$3,000 in unexpected repairs.”

- Show real examples. Use visual aids, customer testimonials, or short videos that demonstrate how products protect owners in real-world scenarios.

- Connect the dots. Relate every product back to the customer’s personal situation—mileage, driving style, and ownership plans.

Value-based presentations increase perceived benefit, reduce objections, and turn the conversation from cost to protection.

4. Ignoring the Digital Experience

Today’s buyers are doing more of their financing research online. According to Cox Automotive, over 70% of car buyers now prefer to complete at least part of their F&I process digitally. Yet many dealerships still rely entirely on in-person, paper-based presentations.

That disconnect creates friction. When a customer moves from a seamless online shopping journey to a manual, lengthy F&I process, it feels outdated and frustrating.

How to fix it:

AVA® pulls soft-inquiry credit and full bureaus before F&I, so deals get structured to fund. Take the tour.

- Integrate digital F&I tools. Allow buyers to explore payment options, warranty details, and credit terms online before they visit the dealership.

- Use virtual presentations. For remote buyers or busy customers, provide digital F&I sessions through secure video or screen-share platforms.

- Automate credit pre-qualification. With tools like AVA™ Credit, customers can pre-qualify instantly without affecting their credit score. This not only improves transparency but also speeds up the in-store experience.

Digital F&I doesn’t replace human connection, it enhances it. By aligning online convenience with in-store expertise, dealerships can deliver the hybrid buying experience modern shoppers expect.

5. Forgetting to Build Trust

At its core, F&I is about trust. Customers are making major financial commitments, often while feeling anxious about hidden fees or upsells. If the process feels rushed, opaque, or overly sales-driven, trust breaks down quickly.

How to fix it:

- Be transparent about costs. Present all fees, rates, and options clearly. Hidden costs are the fastest way to lose credibility.

- Position yourself as an advisor, not a seller. Frame your recommendations as guidance designed to protect the customer’s purchase, not to pad the dealership’s profits.

- Follow up after delivery. A simple check-in or thank-you call reinforces care and builds long-term loyalty.

When trust is established, customers not only buy more F&I products but also become vocal advocates for your dealership.

Frequently Asked Questions About F&I Presentations

What are the most common F&I presentation mistakes?

The big five are information overload, generic scripts, leading with price, ignoring digital tools, and neglecting trust. These issues block decisions, create friction, and reduce product uptake.

How do I avoid overwhelming customers with information?

Prioritize relevant products, use plain language, and simplify the menu. Start with two or three top recommendations, explain terms like GAP in simple words, and tie options to how the customer drives.

How can I personalize F&I without slowing things down?

Use your CRM, digital retail tools, and credit insights to tailor the pitch. Pre-qualify with AVA™ Credit to understand budget and risk early, then align tone, pace, and product fit by buyer type.

Why should I present value before price in F&I?

Price-first triggers resistance. Lead with outcomes, such as average savings on repairs, and show real examples or testimonials. Connect benefits to mileage, driving style, and ownership plans before sharing the cost.

What does a modern digital F&I experience include?

Offer online exploration of payments, warranties, and credit terms, plus virtual F&I sessions for remote or busy buyers. Automate pre-qualification with tools like AVA™ Credit to speed up in-store steps and improve transparency.

The Bottom Line

Your F&I presentation can make or break the profitability and reputation of your dealership. The most successful F&I managers focus less on memorized pitches and more on authentic, customer-centric conversations.

By avoiding these five common mistakes, overloading customers, using generic scripts, leading with price, ignoring digital tools, and neglecting trust—you can create an F&I process that is faster, more transparent, and more profitable.

As the automotive industry continues to evolve with AI and digital retailing, F&I departments must evolve too. Tools like AVA Credit help bridge that gap by giving dealerships instant pre-qualification, improved compliance, and a smoother customer experience.

Dealers who modernize their F&I approach today are setting the stage for stronger customer relationships and higher profitability tomorrow.