Most internet leads look strong on the surface, then stall the moment money enters the conversation. The issue usually isn’t interest, it’s uncertainty. Your team is forced to sell without knowing creditworthiness, payment comfort, or trade equity.

Dealers across North America tell us the same thing: lead volume is high, but true deal-ready opportunities are not.

This article breaks down why traditional internet leads fail, what automotive credit insights software actually delivers, and how a credit-first approach turns basic form-fills into lender-ready deals—without forcing you to rebuild your workflow.

Most internet leads break down for one reason: the first real money conversation happens too late.

Your team schedules appointments, shows vehicles, and builds momentum—then discovers in-store that the shopper can’t be approved on that unit, or can’t live with the payment. By then, both sides have invested time, and restarting the process feels like starting over.

Without automotive credit insights software, BDC and sales teams end up treating every lead the same:

Same templates

It might feel consistent, but it’s not efficient. High-intent, credit-ready buyers sit in the same queue as low-intent shoppers, and your marketing budget gets burned chasing deals that were never realistic on those terms.

A typical lead gives you just enough to start a conversation: name, contact info, and a vehicle of interest. What it doesn’t give you is the context that determines whether the deal can actually happen.

Most teams are missing:

A usable credit picture

That gap creates operational drag. Reps spend hours calling, texting, and emailing leads who may not qualify, may have negative equity, or may be anchored to a model their income and credit won’t support. Payments get quoted based on ideal assumptions, then the structure has to be rebuilt once credit is finally reviewed.

From the shopper’s perspective, it’s just as frustrating. They form expectations online—often based on optimistic payment ads—then get told later the numbers have to change. That disconnect drives no-shows, cancellations, and “not transparent” reviews.

It also shows up in ROI. If close rates are low and cycles are long, cost per sale rises. You can buy more leads—or you can make each lead more workable by adding financial context earlier.

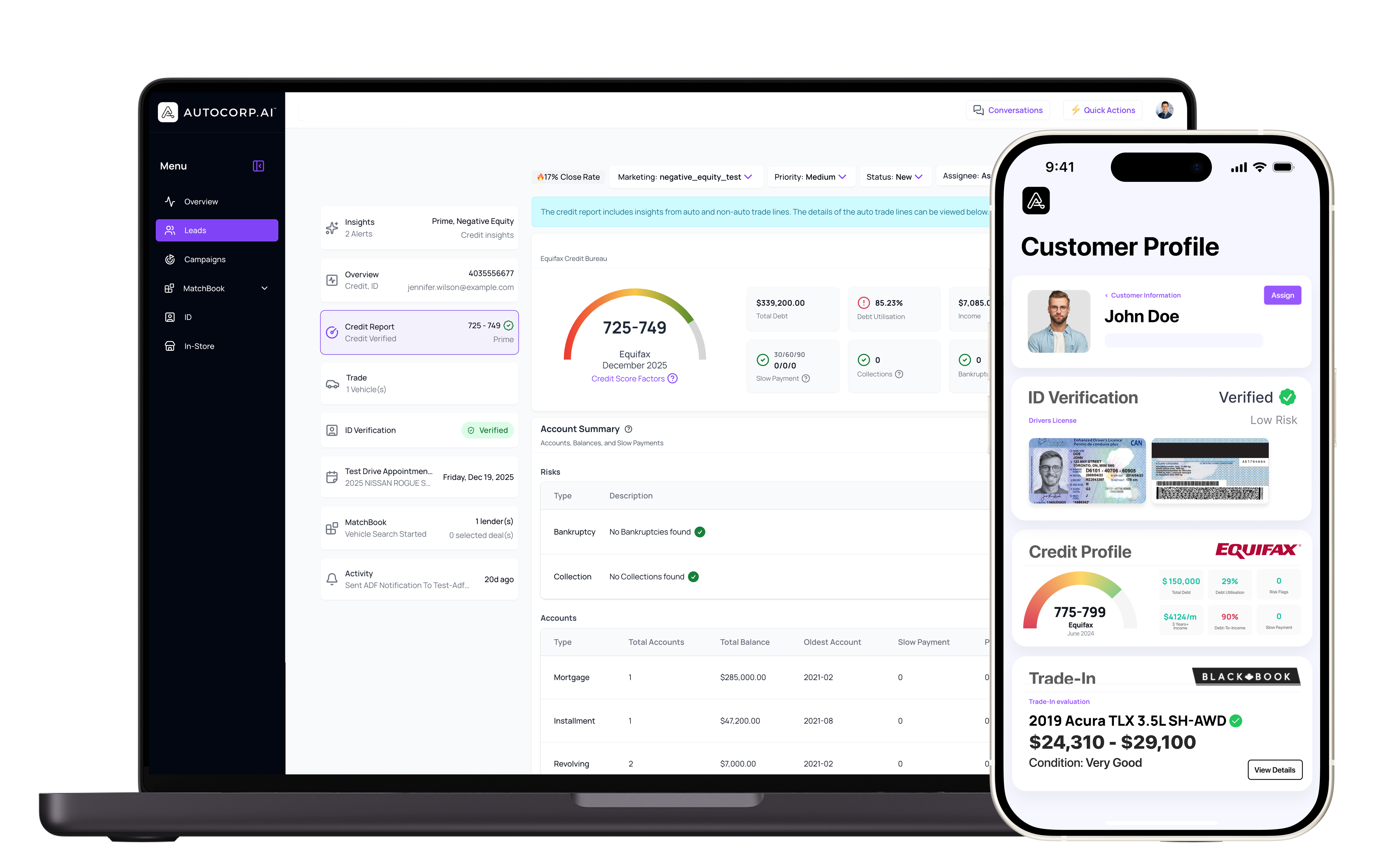

Automotive credit insights software fills in the missing financial picture early, without forcing the shopper through a full credit application up front.

In simple terms, it can capture and infer soft credit insights, income estimates, and payment preferences while the customer is online, then use that information to guide realistic, lender-aware deal structures before they visit the dealership.

Instead of receiving a lead and asking, “Can this person buy?”, your team can start with, “What can this person buy confidently and comfortably?”

When credit insights are attached to the lead, your team can respond with more accurate direction, such as:

Recommending specific vehicles that align with approval odds

With Autocorp.ai, these insights are designed to arrive alongside the lead and fit into the tools you already use—so you can act faster without adding friction for the shopper.

Once leads arrive with automotive credit insights, the workflow can change immediately.

BDC and sales teams can prioritize follow-up by readiness, not just time stamp. Leads that are structurally sound rise to the top, so your best effort goes to the deals most likely to close.

Pre-structured, credit-aware deals also shorten the desk and F&I process. When sales, F&I, and lenders start from a realistic structure, there’s less back-and-forth, fewer rehashes, and fewer surprise declines. Approvals tend to move faster, and deliveries feel smoother.

Credit insights also improve inventory alignment. Instead of presenting aspirational models that won’t pencil, your team can quickly focus on vehicles that match the shopper’s approval profile and budget. That builds trust and keeps the conversation centered on options you can actually deliver.

The benefits show up in the KPIs dealers care about:

Higher show rates, because expectations are grounded early

A common concern is: “Is this going to force us to change everything?”

It shouldn’t. The best automotive credit insights software supports the way your dealership already works. The goal is to enrich what hits your CRM, desking, and digital retailing tools—so your team operates with clarity instead of guesswork.

Autocorp.ai is built to plug into existing workflows so leads can arrive enriched with credit insights, trade-in details, and payment preferences. Your BDC can quickly spot who’s closest to deal-ready. Your desk can start from cleaner structures that are more likely to be accepted by lenders.

That also benefits your lender relationships across automotive, RV, marine, and powersports. Cleaner structures up front typically mean fewer declines and fewer last-minute changes. Over time, that supports more predictable, more efficient lender performance.

A credit-first approach can also improve the customer experience when it’s done correctly.

Using soft-pull credit, clear disclosures, and transparent payment options helps reduce surprises later in the process. Shoppers feel like the dealership was upfront about what’s realistic, and your team has better documentation of how numbers were formed.

The end goal isn’t to “sell credit.” It’s to remove uncertainty early so the right customer lands on the right vehicle, at a payment they can live with, with a structure a lender will actually fund.

Without financial context, internet leads are educated guesses. Your team has to work harder to find the real deals inside them, and many opportunities never surface because the money conversation starts too late.

With automotive credit insights software, those same leads arrive as near-deal-ready opportunities that can be prioritized, structured, and closed more efficiently.

The next step is to pressure-test your own lead flow:

How many appointments don’t show because expectations were off?

Moving to a credit-first, online-to-showroom experience doesn’t require a new store or a new tech stack. It requires better insight delivered inside the tools you already rely on—so every lead has a clearer path to a real approval.

No. It’s designed to add early clarity (approval likelihood, payment range, deal direction) so you’re not waiting until the end of the process to find out the deal won’t work.

It shouldn’t. The point is to keep the shopper experience simple while giving your team richer context in the background—so you get better leads, not fewer leads.

It helps BDC teams prioritize and personalize follow-up. Instead of generic scripts for every lead, reps can tailor the first response to realistic vehicles and payments, which increases engagement and appointment quality.

A strong credit insights platform should integrate into what you already use. The value comes from enriching your existing workflow, not forcing your team to learn a brand-new process.

Equip your team with the data they need to confidently approve more deals and reduce risk using our automotive credit insights software. At Autocorp.ai, we help lenders and dealers translate complex credit data into clear, actionable decisions. If you are ready to modernize your credit workflows and deliver a smoother experience for your customers, reach out and contact us today.