Activix

Activix  AutoTrader

AutoTrader  Black Book

Black Book  CarGurus

CarGurus  Equifax

Equifax

In today’s automotive market, great inventory and strong salespeople are only part of the equation. The real driver behind dealership performance is financing.

With rising interest rates, stricter lending criteria, and more informed buyers, traditional finance processes are no longer enough. Customers expect speed, transparency, and options. Dealers who modernize their approach to auto financing are seeing higher approval rates, faster deal flow, and stronger customer satisfaction.

If your goal is to close more sales in a competitive environment, it’s time to rethink your dealership’s financing strategy.

Key Takeaways

- Modern dealership financing works best when you start with early pre-qualification (including soft credit pulls) so buyers know their budget before choosing a vehicle.

- Approval-based vehicle matching reduces failed deals by showing only vehicles that fit lender guidelines and the customer's credit profile.

- A broader lender network helps raise approval rates, especially for near-prime and subprime buyers who need more flexible programs.

- Digital financing options (online apps, document upload, clear payment ranges) reduce delays and improve buyer confidence.

- Tracking finance metrics (approval rates, gross per deal, lender speed, restructure frequency) helps the F&I team adjust strategy and close faster.

Why Traditional Dealership Financing Is Losing Ground

For years, the financing process followed a predictable pattern: gather the customer’s information, submit it to lenders, wait for a response, and structure the deal afterward.

That model creates friction in today’s market.

Modern buyers expect:

- Immediate answers

- Clear payment expectations

- Digital convenience

- No surprises late in the deal

At the same time, lenders have tightened risk policies. Debt-to-income ratios, loan-to-value limits, and documentation standards are more scrutinized than ever.

The result? Delays, restructured deals, and frustrated customers.

To compete effectively, dealerships must move financing from a back-end function to a strategic sales advantage.

1. Start with Pre-Qualification and Soft Credit Pulls

One of the most impactful changes a dealership can make is introducing pre-qualification early in the customer journey.

Instead of waiting until the buyer selects a vehicle, soft credit pull technology allows you to understand buying power upfront without affecting the customer’s credit score.

With solutions like AVA™ Credit, dealerships can:

- Instantly assess credit tiers

- Set realistic payment expectations

- Match buyers with appropriate lenders

- Reduce last-minute deal breakdowns

When customers know what they qualify for early in the process, trust increases. Sales conversations become more productive. Approval rates improve because deals are structured correctly from the start.

Pre-qualification transforms financing from a hurdle at the end into a tool that supports the sale from the beginning.

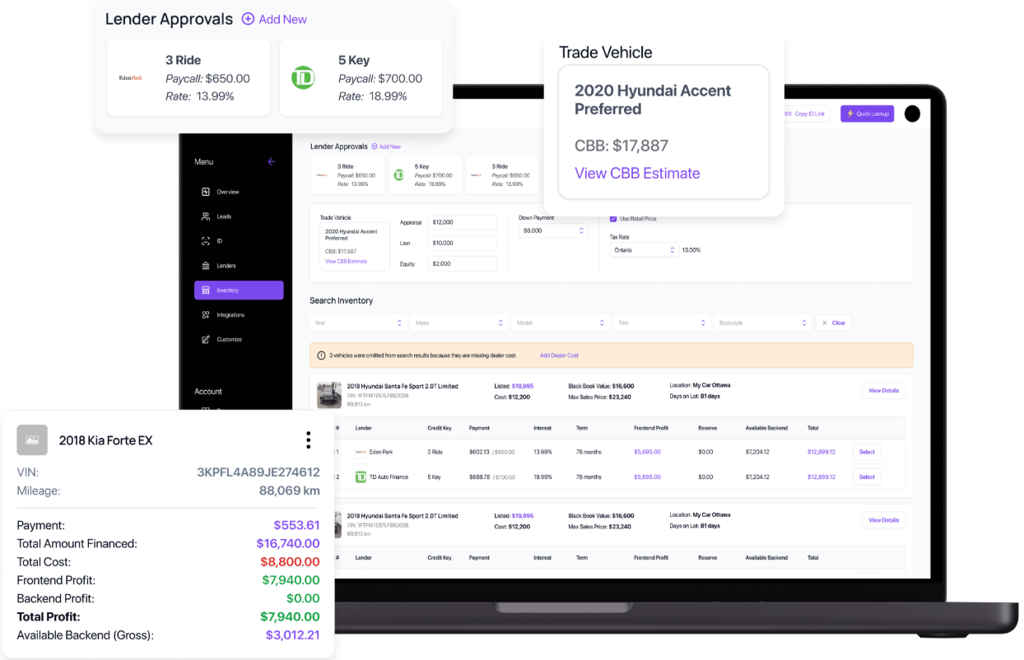

2. Use Approval-Based Vehicle Matching

A common reason deals fall apart is simple: customers are shown vehicles that don’t align with lender approvals.

Excitement builds around a vehicle, only for financing to derail the transaction at the desk.

Approval-based vehicle matching solves this problem.

By combining credit insights with real-time inventory data, dealerships can present only financing-ready options. This ensures that every vehicle shown is realistically purchasable based on lender guidelines.

The benefits are significant:

- Fewer turn-downs

- Less time restructuring deals

- Faster closings

- Improved gross retention

When sales teams align inventory with actual approval conditions, the buying process becomes smoother and more predictable.

3. Expand Your Lender Network Strategically

In today’s environment, relying on a narrow group of traditional A-credit lenders limits your opportunity.

A large portion of buyers fall into near-prime or subprime categories. Many are fully capable of vehicle ownership but require structured programs tailored to their credit profile.

AVA® pulls soft-inquiry credit and full bureaus before F&I, so deals get structured to fund. Take the tour.

Dealerships that expand their lender network can:

- Serve a broader customer base

- Increase approval rates

- Offer flexible term options

- Reduce lost deals due to rigid criteria

Technology platforms like AVA™ Credit support intelligent lender routing, helping match each applicant to lenders most likely to approve based on real-time data.

This reduces guesswork for your F&I team and speeds up the path from application to approval.

4. Deliver a Seamless Digital Financing Experience

Consumers now expect the ability to complete much of the car-buying process online, including financing.

A digital-first financing workflow allows buyers to:

- Submit credit applications online

- Upload required documents

- Receive approvals faster

- Understand payment structures before visiting the showroom

Dealerships that offer a modern digital experience capture leads 24/7 and reduce overall time-to-delivery.

More importantly, digital financing builds credibility. Buyers perceive your dealership as transparent, efficient, and customer-focused.

In a competitive market, convenience can be the deciding factor.

5. Optimize the Finance Desk with Data

Innovative financing isn’t just about tools, t’s about insight.

High-performing dealerships track key finance metrics such as:

- Approval rates by credit tier

- Average gross per deal

- Lender funding speed

- Restructured deal frequency

- Closing ratios tied to payment ranges

With AVA™ Credit, dealerships gain access to performance reporting that highlights lender trends and credit patterns. This data empowers finance managers to adjust strategy in real time.

When you understand which lenders are more flexible with specific buyer profiles, you can structure deals smarter and faster.

Data-driven finance desks consistently outperform reactive ones.

How AVA™ Credit Strengthens Your Financing Strategy

Financing is often the true engine behind dealership profitability. AVA™ Credit was designed to modernize and streamline that engine.

Key capabilities include:

- Soft Pull Pre-Qualification: Instant credit insights with no impact to scores

- Intelligent Lender Matching: Route applications to lenders most likely to approve

- Approval-Based Inventory Alignment: Show buyers vehicles they can realistically finance

- Faster Application-to-Approval Time: Reduce delays and close before customers shop competitors

- Performance Reporting: Track F&I metrics and lender trends to continuously improve

By integrating credit intelligence directly into your workflow, AVA™ Credit helps dealerships convert more applications into approvals—and more approvals into delivered vehicles.

Financing Innovation Drives Sales Growth

In today’s automotive landscape, financing is no longer just a support function. It is a competitive differentiator.

Dealerships that embrace innovative auto financing strategies:

- Close more deals

- Reduce friction in the buying process

- Improve customer satisfaction

- Increase long-term profitability

By combining pre-qualification, smarter lender matching, digital workflows, and real-time data insights, you can transform financing from a bottleneck into a growth engine.

The dealerships winning today are not necessarily working harder. They’re financing smarter.