Activix

Activix  AutoTrader

AutoTrader  Black Book

Black Book  CarGurus

CarGurus  Equifax

Equifax

If you're a sales manager or GM at a small-to-mid-sized dealership, you already know the gut-drop feeling of realizing a deal was fraudulent after the vehicle has left the lot. By then, the damage is done—and it's expensive.

The numbers across North America are alarming. According to Equifax Canada's H1 2024 Fraud Trends Report, automotive fraud jumped 54% year-over-year, with nearly 48.3% of all flagged applications involving identity fraud as of Q2 2024. South of the border, the FTC received over 60,000 auto fraud complaints in 2024 and is on pace to shatter that record in 2025, with a 43% increase in complaints in Q1 2025 alone. Synthetic identity fraud is surging on both sides of the border, with Point Predictive's 2025 Auto Lending Fraud Trends Report putting the total auto lending fraud risk at $9.2 billion across North America—the highest ever measured.

The hard truth? Most dealerships discover they've been defrauded long after the vehicle is gone. The good news is that the tools to stop it before it happens exist right now.

Here's what actually works—including where technology like AVA™ ID can do the heavy lifting your team shouldn't have to do manually.

Key Takeaways

- Identity fraud is the most common auto fraud pattern across North America, and synthetic identity fraud is growing fast.

- Dealerships lower risk by verifying government ID, using biometric checks, and running a soft credit pull early.

- Fraud prevention works best when staff verify employment, watch for synthetic identity red flags, and confirm test drives before releasing keys.

- Remote buyers and third-party financing deserve extra review because they remove the in-person checks that catch many bad deals.

- Strong records, clear escalation rules, and regular staff training make fraud easier to spot and document.

What's at Stake: A Quick Reality Check

Before diving into the steps, let's put a number on the risk. A dealership selling 50 vehicles per month at an average profit of $2,500, with a conservative 3.5% fraud rate, is looking at roughly $6,125 in monthly losses—or over $73,000 per year—when you factor in legal fees, chargebacks, and administrative costs. That's not a rounding error. That's a salesperson's annual salary.

The 12 Steps

1. Require Two Forms of ID—and Actually Examine Them

This sounds obvious, but "requiring ID" and verifying ID are two different things. Require a government-issued photo ID (driver's license or passport) plus a secondary proof of address—a utility bill, bank statement, or government correspondence.

More importantly, train your staff to look at IDs critically. Holograms that don't shift under light, fonts that look slightly off, laminate that's bubbling at the edges—these are real tells. In the U.S., the FBI's identity document fraud resources and your state's DMV guidelines are good starting points. In Canada, the RCMP's document verification resources and provincial motor vehicle authority guides serve the same purpose.

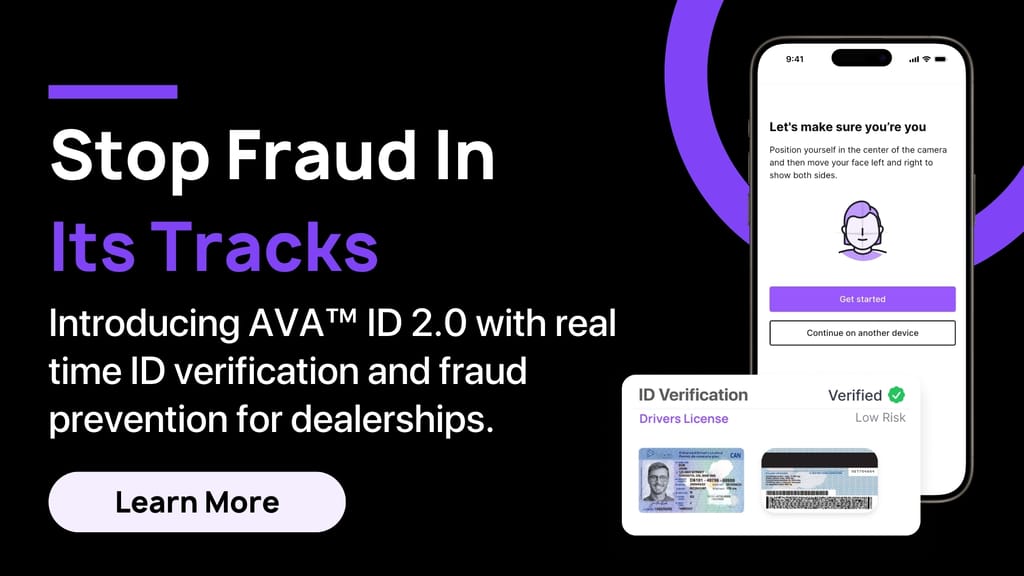

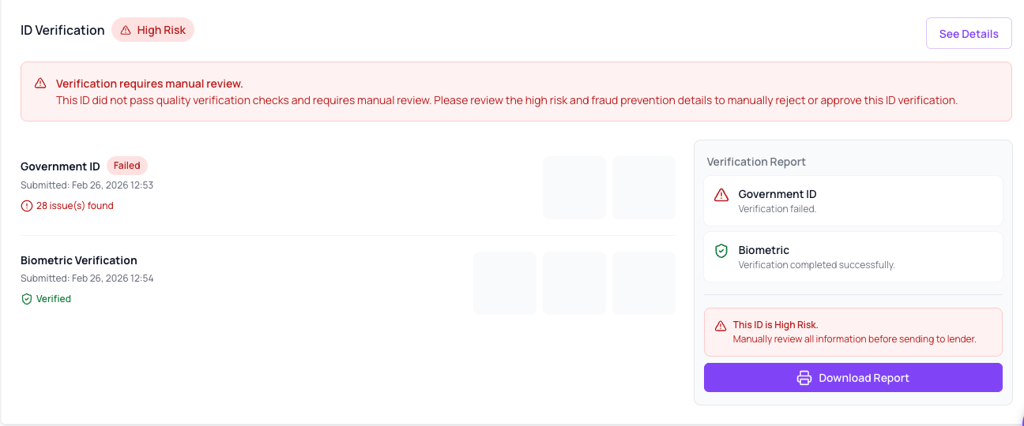

The faster fix: AVA™ ID verifies government IDs in seconds—extracting name, address, date of birth, ID number, and expiry date automatically. What takes a trained staff member several minutes of careful examination happens in under 10 seconds, with greater consistency.

2. Add Biometric Verification to Your Process

A fraudster with a stolen or fabricated ID can pass a visual check. What they can't easily fake is a live biometric match.

Biometric verification—specifically liveness detection combined with facial recognition—confirms that the person holding the ID is the same person standing in front of you (or submitting remotely). It's the difference between checking a piece of plastic and confirming a human being.

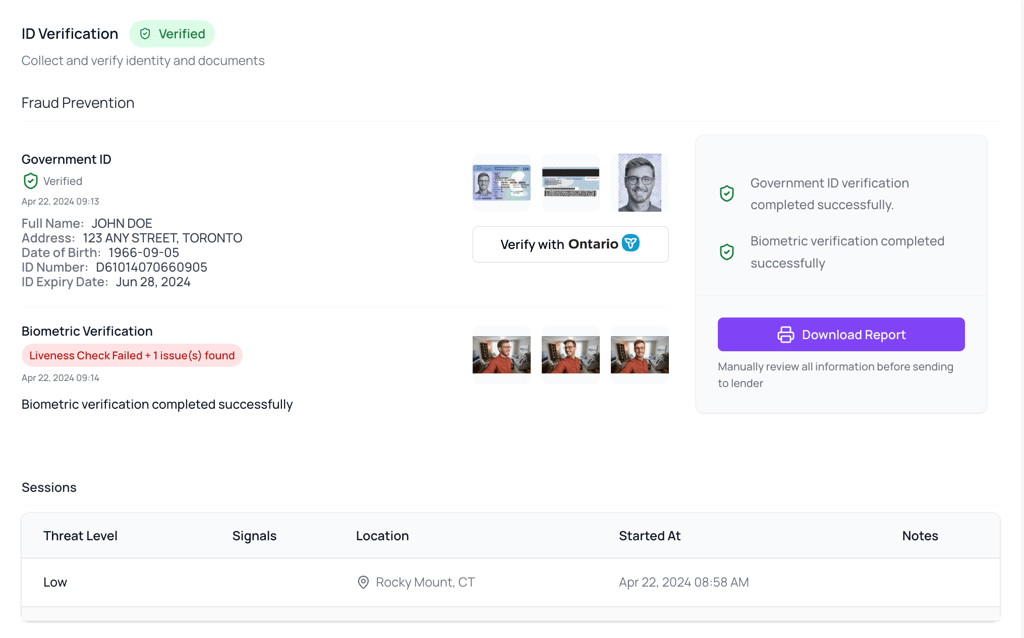

How AVA™ ID handles this: AVA™ ID's biometric matching runs a liveness check alongside the government ID verification. The system flags mismatches before your team even sees the lead. You get a clear "Verified" or “Failed” status, with the government ID images and biometric confirmation stored securely in the lead record—ready to share with lenders if needed.

"Is this customer legitimate?" — This is one of the most common questions dealers ask. AVA™ ID answers it in seconds, not minutes.

3. Run a No-Impact Credit Check Before Investing Time in the Deal

Here's a scenario that plays out in dealerships every week: a salesperson spends two hours with a customer, gets emotionally invested in the deal, and only then discovers the credit application doesn't hold up. That's two hours gone, and a potential fraud attempt that could have been caught at the door.

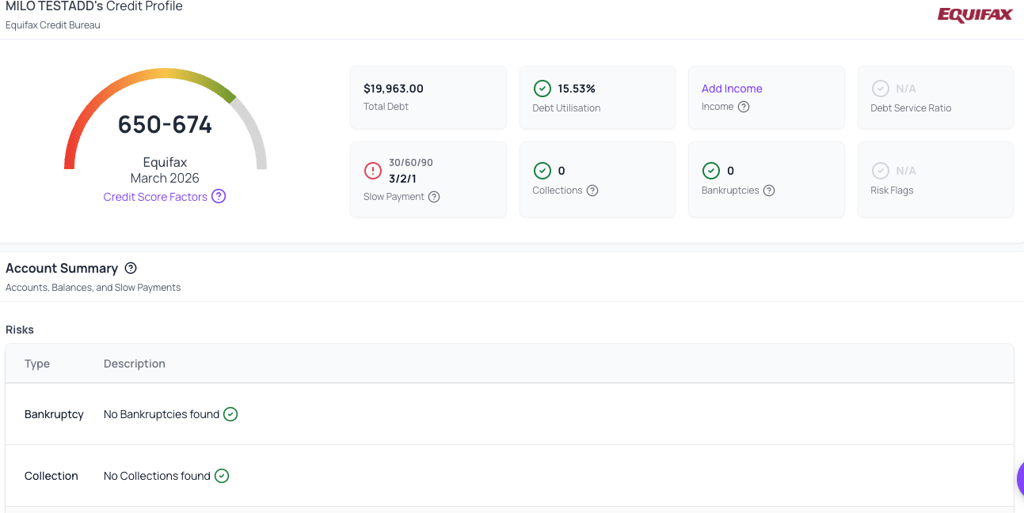

AVA™ Credit (powered by Equifax) lets you run a soft credit pull—no impact to the customer's score—right at the start of the conversation. You get an Equifax credit score and early signals about whether the application is consistent with the customer's actual financial profile.

Why this matters for fraud prevention: Synthetic identity fraud often produces credit profiles that look thin or inconsistent. A soft pull surfaces those anomalies before you've committed time, resources, or inventory to the deal.

4. Watch for Synthetic Identity Red Flags on Applications

Synthetic identity fraud is the fastest-growing fraud type in auto lending on both sides of the border. In Canada, Equifax Canada reported incidents nearly tripling—from 2.8% in Q2 2023 to 8% in Q2 2024. In the U.S., Point Predictive found that nearly 1 in every 114 auto loan applications now involves a fabricated identity—more than double the rate from 2020.

Criminals combine a real government ID number (a Social Security Number in the U.S., a Social Insurance Number in Canada—often stolen from someone with little credit history, like a child, a recent immigrant, or a deceased person) with fabricated personal details to create a "new" identity.

Red flags to train your team to spot:

- Name/address inconsistencies: Small variations in spelling across documents, or an address that doesn't match the ID

- Thin credit file with high income claims: A customer claiming $120K annual income but with almost no credit history

- Recently established credit: A profile that shows all accounts opened within the last 6–12 months

- Mismatched employment details: Employer names that are slightly off, or phone numbers that don't match the company

When you see two or more of these together, slow down. Call the employer directly—don't use the number on the application.

For example, When a verification doesn't pass cleanly, AVA™ ID surfaces the issue immediately rather than silently failing.

The customer receives a link via SMS or email and completes a three-stage process: Link Opened → Verification In Progress → Verification Completed. During that process, they scan their government-issued ID (front and back) and complete a biometric liveness check—a real-time selfie that confirms the face on the ID matches the person submitting it.

If the document appears tampered with, the biometric doesn't match, or the liveness check fails, the verification returns a "Failed" status instead of a clean "Verified." The dealer gets a real-time alert the moment it happens.

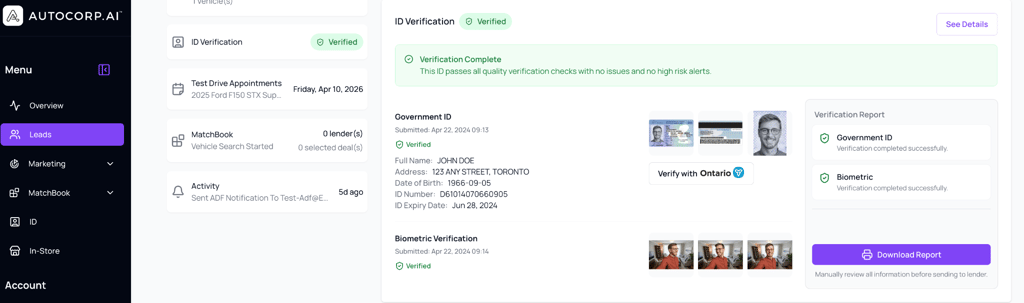

Every outcome is timestamped, encrypted, and stored in the lead record—exportable as a full IDV report for lenders or law enforcement in seconds.

Related reading: Canadian Auto Fraud Soars: Identity Theft and Falsified Credit Applications Drive 54% Surge

5. Verify Employment and Income Directly

Don't rely solely on what's written on the application. Call the employer. Ask for HR or payroll. Confirm the person's name, title, and employment status.

This takes about five minutes and catches a surprising number of fraudulent applications. Fraudsters count on dealerships being too busy or too eager to close to make that call.

A few things to check:

- Does the employer's phone number match what's publicly listed for the company?

- Does the person answering confirm the applicant works there, or do they seem confused?

- Is the income figure consistent with the stated role and industry?

For self-employed applicants, ask for two years of tax returns—IRS Form 1040 with W-2s in the U.S., or a Notice of Assessment from the CRA in Canada. Both are significantly harder to fabricate convincingly than a pay stub.

Worth noting: Point Predictive's 2025 report found that income and employment misrepresentation alone accounts for 43% of total auto fraud risk exposure—$3.9 billion of the $9.2 billion total. Calling the employer is one of the cheapest fraud checks available.

6. Secure Your Test Drives

Vehicle theft via fraudulent test drives is a real and growing problem. A fraudster books a test drive, presents a fake or stolen ID, takes the vehicle, and disappears. By the time you realize what happened, the car is gone.

The standard process—photocopying a license and handing over keys, is not enough.

How AVA™ ID integrates with test drives: AVA™ VeriDrive requires customers to complete identity verification before a test drive is confirmed. The customer submits their ID and completes a biometric check from their phone. Your team gets a verified status before the keys leave the hook.

650+ dealerships across North America use this process. It doesn't slow down the customer experience—it actually builds trust, because legitimate buyers appreciate knowing the dealership takes security seriously.

Related reading:How AVA™ ID Stops Fraud Before It Hits Your Desk

7. Apply Extra Scrutiny to Remote and Out-of-State/Province Buyers

Remote deals aren't inherently suspicious—but they do remove the in-person verification layer that catches a lot of fraud. When a buyer is purchasing from another state, province, or country, you need to compensate for that gap.

See how 650+ dealerships use AVA® to surface credit-qualified buyers before they sit down at the desk.

Practical steps for remote buyers:

- Video verification: Conduct a live video call where the customer holds their ID up to the camera. Record it with consent.

- Additional documentation: Request two forms of ID plus proof of address, not just one.

- Avoid sight-unseen deals at above-market prices: If someone is offering to pay full asking price without seeing the vehicle and wants to arrange their own transport, that's a pattern worth pausing on.

- Use AVA™ ID remotely: AVA™ ID works via SMS or email link—the customer completes verification from their own device, and you get the result in your dashboard. No in-person requirement.

8. Be Cautious with Third-Party Financing

Third-party financing arrangements—where a buyer claims to have financing arranged through a company you haven't worked with before—deserve extra verification steps.

Before proceeding:

- Confirm the financing company is legitimate and licensed in your state or province

- Verify their contact information independently (not from documents the buyer provides)

- Understand their verification procedures and whether they've confirmed the buyer's identity

- Be wary of deals where the third-party funder is pushing urgency

Legitimate financing companies don't pressure dealerships to skip steps.

9. Build a Suspicious Activity Reporting System

Your frontline staff are your first line of defense, but only if they know what to look for and have a clear path to escalate concerns without feeling like they're killing a deal.

Build a simple internal process:

- A defined list of red flags (use this article as a starting point)

- A clear escalation path: who to tell, how quickly, and what information to capture

- A no-blame culture around flagging concerns—staff shouldn't feel penalized for slowing down a suspicious deal

Document every suspicious interaction, even if it doesn't result in a confirmed fraud attempt. Patterns matter, and law enforcement can use this information.

10. Keep Thorough, Centralized Records

If fraud does occur, your ability to cooperate with law enforcement and potentially recover losses, depends on the quality of your records.

For every deal, store:

- Copies of all IDs presented (front and back)

- The completed credit application

- All customer communications (email, SMS, notes from calls)

- Verification timestamps and outcomes

How AVA™ ID handles this automatically: Every identity verification completed through AVA™ ID is logged, timestamped, encrypted, and stored in a centralized record tied to the lead. You can export a full IDV report— with the option to include completed checks and ID images—in seconds. This is also what lenders want to see when they're reviewing a deal file.

11. Stay Current on KYC and AML Compliance Requirements

Compliance obligations apply whether you're operating in the U.S. or Canada—and the thresholds are nearly identical.

In the U.S., dealerships must file IRS/FinCEN Form 8300 for any cash transaction over $10,000 USD. This is a joint IRS and FinCEN requirement under the Bank Secrecy Act, and it applies specifically to auto dealerships. Failure to file carries civil and criminal penalties.

In Canada, FINTRAC (Canada's financial intelligence unit) requires dealerships to verify customer identity on cash transactions over $10,000 CAD, maintain records of those verifications, and report suspicious transactions.

AVA™ ID is built to meet these standards on both sides of the border. Every verification follows KYC/AML-compliant processes, so your records hold up to regulatory scrutiny without requiring your team to become compliance experts.

Related reading: KYC for Dealers: What FINTRAC Requires in 2025

12. Train Your Team—and Keep Training Them

Fraud tactics evolve. The synthetic identity playbook that worked for criminals two years ago has been updated—Point Predictive found a 644% increase in conversations about AI and deepfakes used for fraud on criminal Telegram channels between 2023 and 2024. Your team's training needs to keep pace.

Practical training approach:

- Quarterly fraud briefings: 30-minute sessions covering new tactics and recent cases from your region

- Role-play verification scenarios: Have staff practice examining IDs and running through the verification workflow until it's second nature

- Clear ownership: Designate one person per shift as the fraud escalation point, someone with authority to slow down or stop a deal

The goal isn't to make your team paranoid. It's to make them confident. A well-trained salesperson can verify a legitimate customer quickly and professionally, which actually improves the buying experience.

Related reading: The Importance of Compliance Training for Dealership Staff

Frequently Asked Questions

What's the most common type of automotive fraud right now?

Across North America, identity fraud dominates. In Canada, Equifax Canada's H1 2024 Fraud Trends Report found identity fraud accounts for 48.3% of all flagged automotive applications—up from 42.9% in Q2 2023. In the U.S., the FTC received over 60,000 auto fraud complaints in 2024, with Q1 2025 already running 43% ahead of that pace. Synthetic identity fraud is the fastest-growing subcategory in both markets.

Does running a credit check for fraud prevention hurt the customer's credit score?

Not if you use a soft pull. AVA™ Credit uses a no-impact soft inquiry through Equifax, so you can check a customer's credit profile at the start of the conversation without affecting their score. This removes a major barrier to early qualification.

How do I verify a customer's identity for a remote or online deal?

AVA™ ID sends a verification link via SMS or email. The customer completes document upload and a biometric liveness check from their own device. You receive the result in your AVA™ dashboard—no in-person requirement, no hardware needed.

What records do I need to keep if I suspect fraud?

Keep copies of all IDs, the full credit application, all communications, and any verification timestamps. AVA™ ID stores all of this automatically and generates exportable IDV reports you can share with lenders or law enforcement.

What should I do if I confirm a fraud attempt?

In the U.S., report it to your local police and file a complaint with the FTC at ReportFraud.ftc.gov. In Canada, contact the Canadian Anti-Fraud Centre at 1-888-495-8501. In both cases, document everything before the trail goes cold and notify the lender immediately if a credit application was involved.

The Cost of Doing Nothing

Fraud doesn't announce itself. It looks like a normal deal, until it isn't. The dealerships that get hit hardest are the ones that assumed their manual process was good enough, or that fraud was someone else's problem.

The math is straightforward: a dealership losing $73,000 per year to fraud, which is a conservative estimate for a 50-unit-per-month operation, could cover the cost of a proper verification platform many times over while protecting every deal in the pipeline.

If you want to see what that looks like in practice, book a demo with the AVA™ team. 650+ dealerships across North America are already using AVA™ ID to verify customers in seconds, meet KYC/AML requirements, and close deals with confidence.

The fraudsters are getting more sophisticated. Your verification process should too.

Related articles: